The 50 30 20 rule is the only budgeting method that doesn’t feel like a punishment.

Let’s be honest: The word “budget” usually sounds terrible. It sounds like a diet. It sounds like you are never allowed to have fun again. It sounds like sitting at the kitchen table with a calculator, crying over a ₹200 coffee.

That is why 99% of people quit budgeting within a month.

But what if I told you that a budget isn’t about restriction? What if it’s actually about permission?

You need a system that manages your money for you, so you don’t have to think about it.

Popularized by Senator Elizabeth Warren, this isn’t a complex accounting trick. It is the golden standard for lazy (smart) people who want to get rich without being miserable.

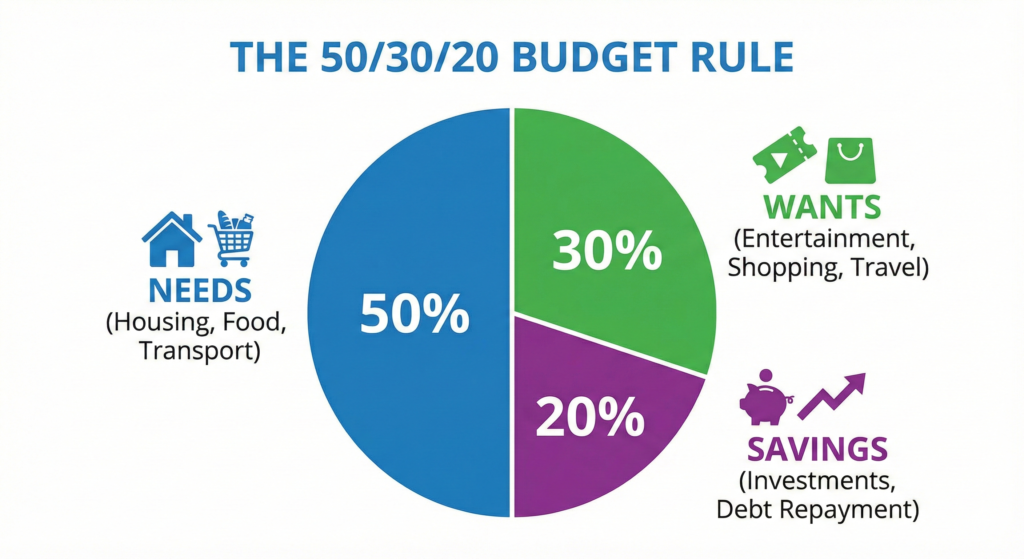

What Is the 50 30 20 Rule?

The concept is incredibly simple. You take your monthly income (after tax) and split it into three buckets.

That’s it. No tracking every transaction. No guilt.

50% → Needs (Survival)

30% → Wants (Fun)

20% → Savings (Freedom)

Let’s break down exactly what goes into each bucket so you can master the 50 30 20 rule.

Bucket 1: 50% for NEEDS

These are the bills you must pay to keep your life running. If you lost your job tomorrow, these are the expenses that would keep you awake at night.

Includes:

- Rent or Home Loan (EMI)

- Groceries (Not restaurants!)

- Electricity and Water bills

- Transport (Fuel/Bus/Metro)

- Insurance premiums

- Basic Medicine

The Trap: Many people mistake “Wants” for “Needs.”

Netflix is not a need. A gym membership is not a need. An iPhone 15 Pro Max is definitely not a need.

If your Needs are over 50% of your income, you have two choices: Downsize your lifestyle (cheaper rent) or increase your income.

Bucket 2: 30% for WANTS

This is the fun bucket. This is why the 50 30 20 rule actually works.

Most budgets fail because they act like robots. Humans need fun. We need to go out, buy nice shoes, and order biryani.

Includes:

- Dining out and ordering in

- Netflix, Spotify, Prime

- Shopping for clothes

- Concerts and Movies

- Travel and Vacations

The Golden Rule: As long as you stay within this 30%, you can spend this money on whatever you want without guilt.

Want to blow it all on a fancy pair of sneakers? Go ahead.

Want to eat out every night? Fine.

Just don’t go over the 30% limit.

Bucket 3: 20% for SAVINGS

This is the most important bucket. This is the difference between being broke at 60 and being wealthy at 40.

This money is not for spending. This money is for your future self.

Includes:

- Emergency Fund: (We’ll cover this next).

- Paying off Debt: High-interest credit cards.

- Investments: Stocks, Mutual Funds, Gold.

This 20% is how you buy Assets instead of Liabilities.

If you can increase this to 30% or 40%, you will reach financial freedom incredibly fast.

Real-Life Example: Salary of ₹50,000

Let’s apply the 50 30 20 rule to a monthly salary of ₹50,000.

- Needs (50%): ₹25,000

- You have ₹25k for rent, food, and bills.

- Wants (30%): ₹15,000

- You have ₹15k to party, travel, and shop.

- Savings (20%): ₹10,000

- You invest ₹10k every month.

Why this is powerful:

If you invest that ₹10,000 monthly for 20 years (at 12% return), thanks to Compound Interest, you won’t just have savings—you will have nearly ₹1 Crore.

All because you followed a simple rule.

How to Automate It (The Secret Sauce)

Willpower is weak. Automation is strong.

Don’t try to “remember” to save.

- Salary Day: Money hits your account.

- Automatic Transfer: Set a standing instruction to move 20% immediately to a separate Investment/Savings account.

- Spend the Rest: Whatever is left is for your Needs and Wants.

As financial expert Ramit Sethi says, “Automate your finances so you can get on with your life.”

Final Thought: It’s a Goal, Not a Law

If you live in a painfully expensive city (like Mumbai or Bangalore), spending only 50% on rent and bills might feel impossible. You might be at 60/30/10.

That is okay.

The 50 30 20 rule is a target.

Start where you are. Maybe you are at 70/20/10 today.

Work to cut the Needs. Work to increase the Income. Slowly push toward that 20% savings goal.

You don’t need a spreadsheet. You just need three buckets.

Quick Action Step:

Open your banking app. Look at last month’s spending.

Roughly calculate:

- How much went to Needs?

- How much went to Wants?

- How much went to Savings?

The numbers might shock you. That shock is the first step to fixing it.

In the next article, we talk about the Emergency Fund—the safety net that stops you from crashing when life hits hard.