If you have ever asked what is compound interest, you are asking the same question Albert Einstein supposedly answered with a warning.

He called it the “Eighth Wonder of the World.”

He said: “He who understands it, earns it… he who doesn’t… pays it.”

In our last article, we met the villain: Inflation, the silent thief stealing your money.

Today, we meet the hero. The weapon you use to fight back.

Compound interest is the only legal way to turn a small amount of money into a massive fortune without winning the lottery. It is the engine behind every rich person’s wealth.

But how does it work? And why is it so powerful?

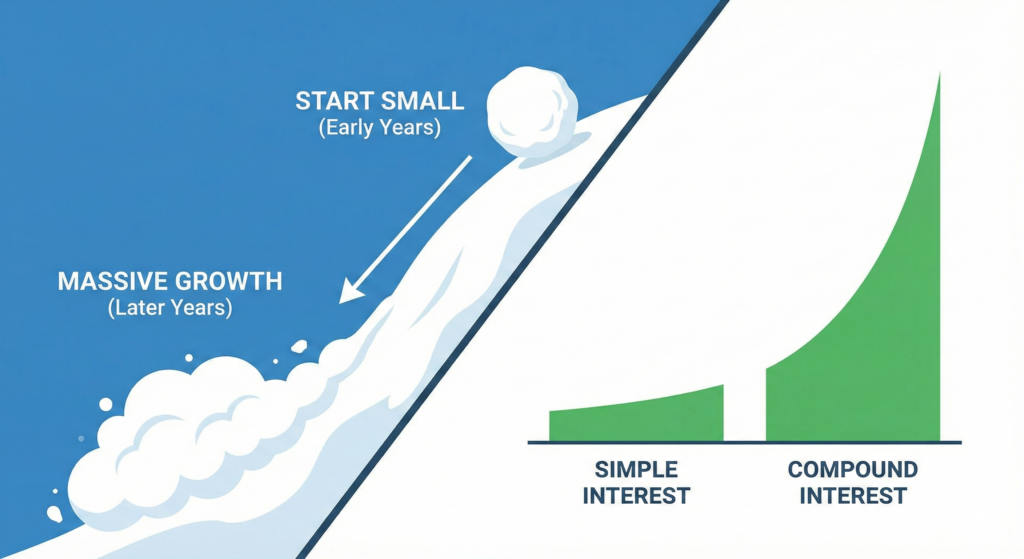

What Is Compound Interest? (The Snowball Effect)

To understand the magic, we first have to look at its boring cousin: Simple Interest.

Simple Interest is when you earn money only on your original investment (the principal).

- You invest ₹100.

- Interest is 10%.

- Year 1: You earn ₹10.

- Year 2: You earn ₹10.

- Year 50: You earn ₹10.

It’s linear. It’s slow. It’s boring.

Compound Interest is different. It is “interest on interest.”

- You invest ₹100.

- Interest is 10%.

- Year 1: You earn ₹10. (Total: ₹110).

- Year 2: You earn 10% on the ₹110. (Total: ₹121).

- Year 3: You earn 10% on the ₹121.

It starts slow. But like a snowball rolling down a hill, it gets bigger, faster, and heavier the longer it rolls.

The Magic in Action: Jack vs. Jill

This is the most famous example in personal finance, but it explains what is compound interest better than any textbook.

Meet Jack and Jill. Both want to retire at age 60.

Jack (The Early Bird):

- Starts investing at age 20.

- Invests ₹5,000 per month.

- Stops at age 30. (Invested for only 10 years).

- Total money invested: ₹6 Lakhs.

Jill (The Procrastinator):

- Starts investing at age 30.

- Invests ₹5,000 per month.

- Continues until age 60. (Invested for 30 years).

- Total money invested: ₹18 Lakhs.

Who has more money at age 60? (Assuming 10% return)

Jack: ₹1.6 Crores

Jill: ₹1.1 Crores

Read that again.

Jack invested 3x less money than Jill, but he ended up richer.

Why? Because his money had 10 extra years to compound.

The 3 Rules of Compounding

To make this “8th Wonder” work for you, you must follow three strict rules.

Rule 1: Time is Everything

The “Compound” part needs time to cook.

In the first few years, the results look pathetic. You will feel like quitting.

- Year 1-5: Boring.

- Year 5-10: Okay.

- Year 10-20: Good.

- Year 20+: Explosive.

The biggest mistake people make is waiting for “more money” to start investing. Start with ₹500. Just start now.

Rule 2: Don’t Interrupt It

Charlie Munger, the billionaire partner of Warren Buffett, famously said:

“The first rule of compounding: Never interrupt it unnecessarily.”

If you pull your money out every time the market crashes or every time you want to buy a new phone, you kill the snowball. You reset the clock to zero.

Let it roll.

Rule 3: The Rate Matters (But Risk Matters Too)

A 2% difference in returns makes a massive difference over 20 years.

- ₹1 Lakh at 6% over 20 years = ₹3.2 Lakhs.

- ₹1 Lakh at 12% over 20 years = ₹9.6 Lakhs.

This is why sticking to a savings account (3%) is dangerous. You need assets like Mutual Funds or Stocks that offer higher returns to fuel the compounding machine.

A Quick Hack: The Rule of 72

Want to do mental math like a genius? Use the Rule of 72.

It tells you how long it takes to double your money.

Formula: 72 ÷ Interest Rate = Years to Double.

- Fixed Deposit (6%): 72 ÷ 6 = 12 Years to double your money.

- Stock Market (12%): 72 ÷ 12 = 6 Years to double your money.

The Dark Side: When Compounding Kills You

Remember Einstein’s quote? “He who doesn’t understand it… pays it.”

Compound interest works both ways.

If you have Credit Card Debt, compounding is your enemy.

Credit cards charge 30-40% interest.

If you owe ₹50,000 and only pay the minimum due, that debt will compound into a mountain that buries you.

Never let compounding work against you.

Final Thought: Plant the Tree

There is an old Chinese proverb:

“The best time to plant a tree was 20 years ago. The second best time is now.”

Understanding what is compound interest changes your perspective. You realize that every ₹100 you spend on junk today isn’t just ₹100 lost—it is the ₹1,000 it could have become in the future.

You have the definition.