You work hard. You save money. You buy a nice car. You buy a bigger house. You buy the latest iPhone.

You look rich.

But at the end of the month, your bank account is empty.

Why?

Because you are buying the wrong things.

Most people think they have a “money earning” problem. Usually, they have a “definition” problem. They don’t know the difference between assets and liabilities.

They spend their lives buying liabilities, thinking they are assets.

If you want to stop living paycheck to paycheck, you need to learn the definition that Robert Kiyosaki (author of Rich Dad Poor Dad) made famous. It is simpler than any accounting textbook.

The Difference Between Assets and Liabilities (Simplified)

If you ask an accountant, they will give you a complicated explanation about balance sheets and depreciation. Sites like Investopedia have great technical definitions, but they can be confusing.

Ignore that for a minute. Here is the only definition that matters for your wallet:

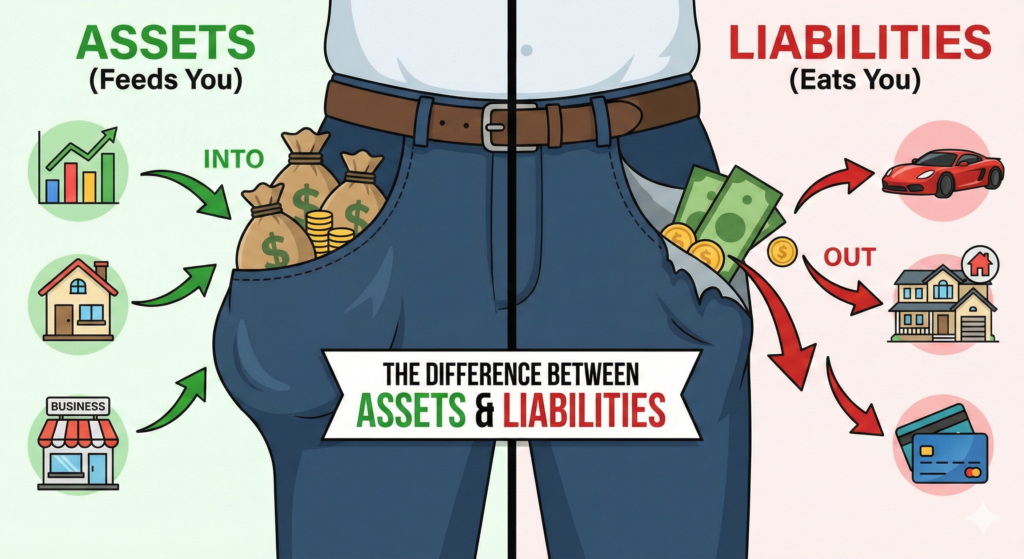

An ASSET puts money IN your pocket.

A LIABILITY takes money OUT of your pocket.

Read that again. This is the core difference between assets and liabilities.

It doesn’t matter how “valuable” something is. It doesn’t matter if your banker calls it an asset.

- Does it pay you? It’s an asset.

- Does it cost you? It’s a liability.

The Middle-Class Trap

This is where 90% of people get stuck. They struggle to see the difference between assets and liabilities in real life. They buy things that look like wealth but actually drain wealth.

The “Car” Trap

You buy a new car for ₹15 Lakhs. You think, “I own an asset worth ₹15 Lakhs!”

Wrong.

- You pay for fuel.

- You pay for insurance.

- You pay for servicing.

- The car loses value (depreciates) the moment you drive it off the lot.

Money is flowing OUT. That car is a liability.

The “House” Controversy

Is your home an asset?

Most people scream “YES!”

But let’s look at the cash flow:

- You pay the mortgage (EMI).

- You pay property tax.

- You pay for repairs.

- You pay for painting.

Unless you rent out a room, that house takes money OUT of your pocket every month.

It is a liability.

(Note: It may become an asset if you sell it for a profit later, but while you live in it, it acts as a liability.)

Examples: Knowing the Difference Between Assets and Liabilities.

To build wealth, you need to shift your spending from Column B to Column A.

| True Assets (Feeds You) | Liabilities (Eats You) |

|---|---|

| Dividend Stocks: Pays you a share of profits. | Luxury Car: Costs fuel, insurance, maintenance. |

| Rental Property: Tenant pays you rent. | Your House: You pay the EMI and repairs. |

| Fixed Deposits: Pays you interest. | Credit Card Debt: You pay the bank interest. |

| Business/Side Hustle: Generates profit. | Subscription Services: Monthly drain on cash. |

| Intellectual Property: Royalties from books/music. | Brand Name Clothes: Lose value instantly. |

The “Rich” Strategy

Rich people and poor people play the game differently because they respect the difference between assets and liabilities.

The Poor Strategy:

Earn Income → Spend on Expenses (Rent, Food) → $0 Left.

The Middle-Class Strategy:

Earn Income → Buy Liabilities (Car, House, Loan) → Expenses → Stuck in the “Rat Race.”

The Rich Strategy:

Earn Income → Buy Assets → Assets Generate More Income → Income Buys Luxuries.

This is the key. The rich do buy Ferraris. But they don’t buy them with their salary. They buy assets first, and they use the profits from the assets to buy the Ferrari.

How to Apply This Today (The Audit)

You don’t need to sell your house or walk to work. But you do need to stop lying to yourself.

If you understand Compound Interest, you know that every rupee you put into a Liability is a rupee that stops working for you.

The Goal:

Get to a point where the income from your Assets covers all the costs of your Liabilities.

That is the definition of Financial Freedom.

Final Thought: Feed the Goose

Imagine you have a goose that lays golden eggs (Assets).

Most people kill the goose to eat it (selling investments to buy a car).

Smart people starve themselves a little bit to buy more geese.

Once you have a flock of geese, you can buy whatever you want with the golden eggs.

In the next article, we will talk about Budgeting—or as I like to call it, “Telling your money where to go instead of wondering where it went.”

Quick Action Step:

Take a piece of paper. Draw a line down the middle.

Left side: Assets (Things that paid you last month).

Right side: Liabilities (Things that cost you last month).

Be honest. If the right side is full and the left side is empty, you know exactly what to fix.