Understanding what is expense ratio is the single most important step for any investor looking to build long-term wealth in India. Many investors focus exclusively on past returns, ignoring the silent drain on their portfolio caused by fund management fees.

In simple terms, an expense ratio is the annual fee charged by mutual fund houses to manage your money. Think of it as the maintenance fee you pay for the professional expertise of a fund manager.

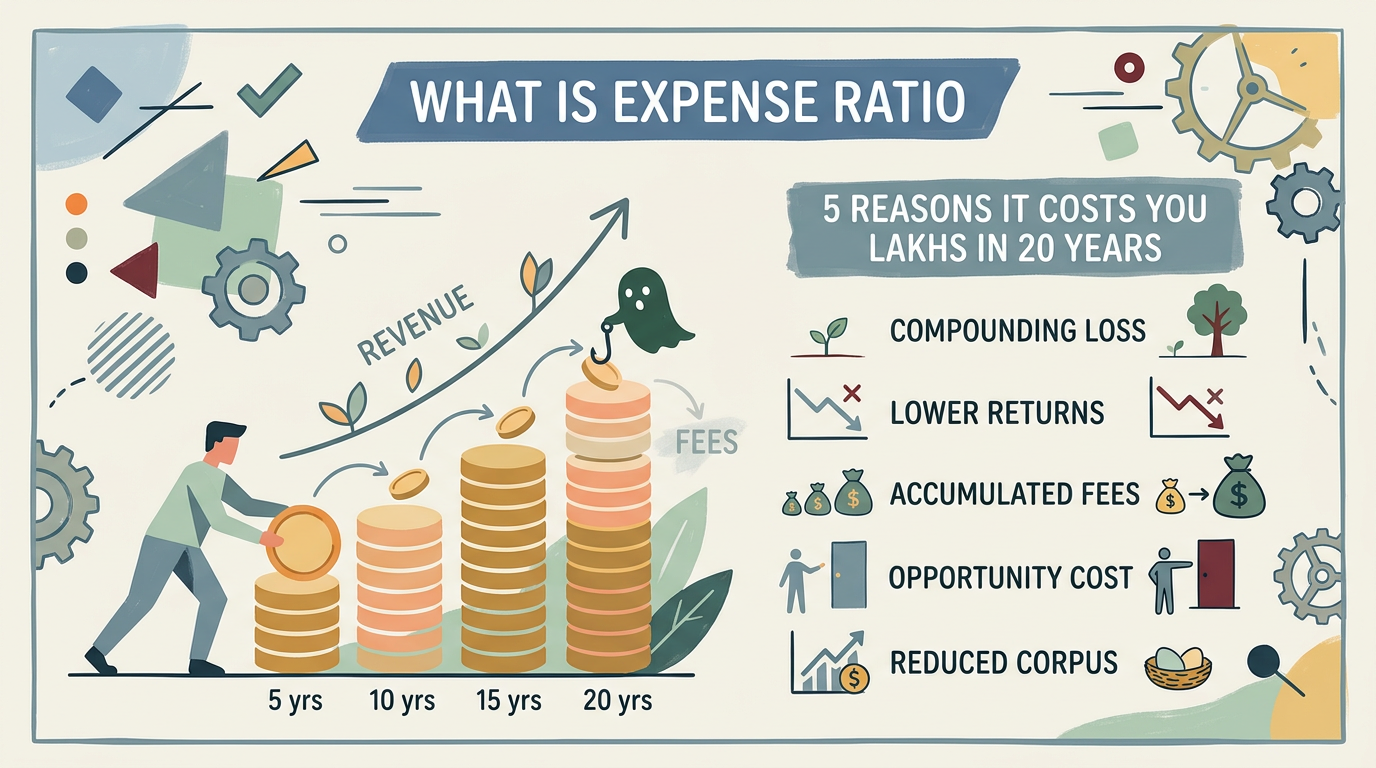

If you want to master your money management strategy, you must understand how these small percentages impact your final corpus. Even a seemingly insignificant 1% difference can cost you lakhs over a two-decade investment horizon.

Why the Expense Ratio Matters for Your Wealth

The expense ratio is deducted directly from the mutual fund’s Net Asset Value (NAV). This means you do not see a separate bill; the fund simply returns a slightly lower amount than the underlying assets earned.

Regulatory bodies like the Securities and Exchange Board of India set caps on these fees to protect retail investors. However, within those caps, fund houses have discretion, and lower is almost always better.

1. The Compounding Impact of High Fees

Compounding is a double-edged sword. While it grows your wealth, it also compounds the impact of fees. If you invest ₹10,00,000 for 20 years at a 12% return, a 1% expense ratio vs. a 2% expense ratio creates a massive gap.

With a 1% expense ratio, your final corpus would be significantly higher than with a 2% ratio. Over 20 years, that 1% difference can result in a shortfall of over ₹5,00,000 to ₹8,00,000 depending on market performance.

2. Understanding Direct vs. Regular Plans

When asking what is expense ratio, you must distinguish between Regular and Direct plans. Regular plans include a commission paid to your distributor or broker, which inflates the expense ratio.

Direct plans cut out the middleman, offering a lower expense ratio. By choosing a Direct plan, you immediately save on commissions, which directly increases your annual returns and long-term wealth.

3. How Expense Ratios Affect Your NAV

The NAV is the price at which you buy or sell mutual fund units. The expense ratio is calculated daily and subtracted from the fund’s assets before the NAV is declared.

Because the deduction happens daily, you are paying the fee every single day you hold the investment. Over time, this daily friction significantly drags down the potential growth of your capital.

4. Active Management vs. Passive Index Funds

Active funds have higher expense ratios because they employ research teams to beat the market. Passive funds, like index funds, have much lower ratios because they simply track a benchmark.

If you are a long-term investor, you must evaluate if the active manager’s outperformance justifies the higher cost. Often, the lower expense ratio of an index fund leads to better net returns.

5. Evaluating the Value Provided by the Fund

Knowing what is expense ratio is only half the battle. You must also look at the fund’s performance net of expenses. A fund with a slightly higher ratio might be worth it if it consistently delivers superior alpha.

Always compare the expense ratio against similar funds in the same category. If a fund charges more but provides no extra value, it is time to reconsider your investment choice.

In summary, what is expense ratio is a question of efficiency. By keeping your costs low, you ensure that more of your money stays invested and continues to compound. Always prioritize low-cost, direct plans to maximize your financial future.