Purchasing an insurance policy is a significant financial commitment. Often, consumers feel pressured by agents to sign documents without fully understanding the terms. Fortunately, the insurance regulator provides a safety net known as the free look period.

Understanding what is a free look period is essential for every policyholder in India. It acts as a cooling-off window, allowing you to review your contract and cancel it if it does not meet your expectations. This protection ensures you are not trapped in a policy that was mis-sold to you.

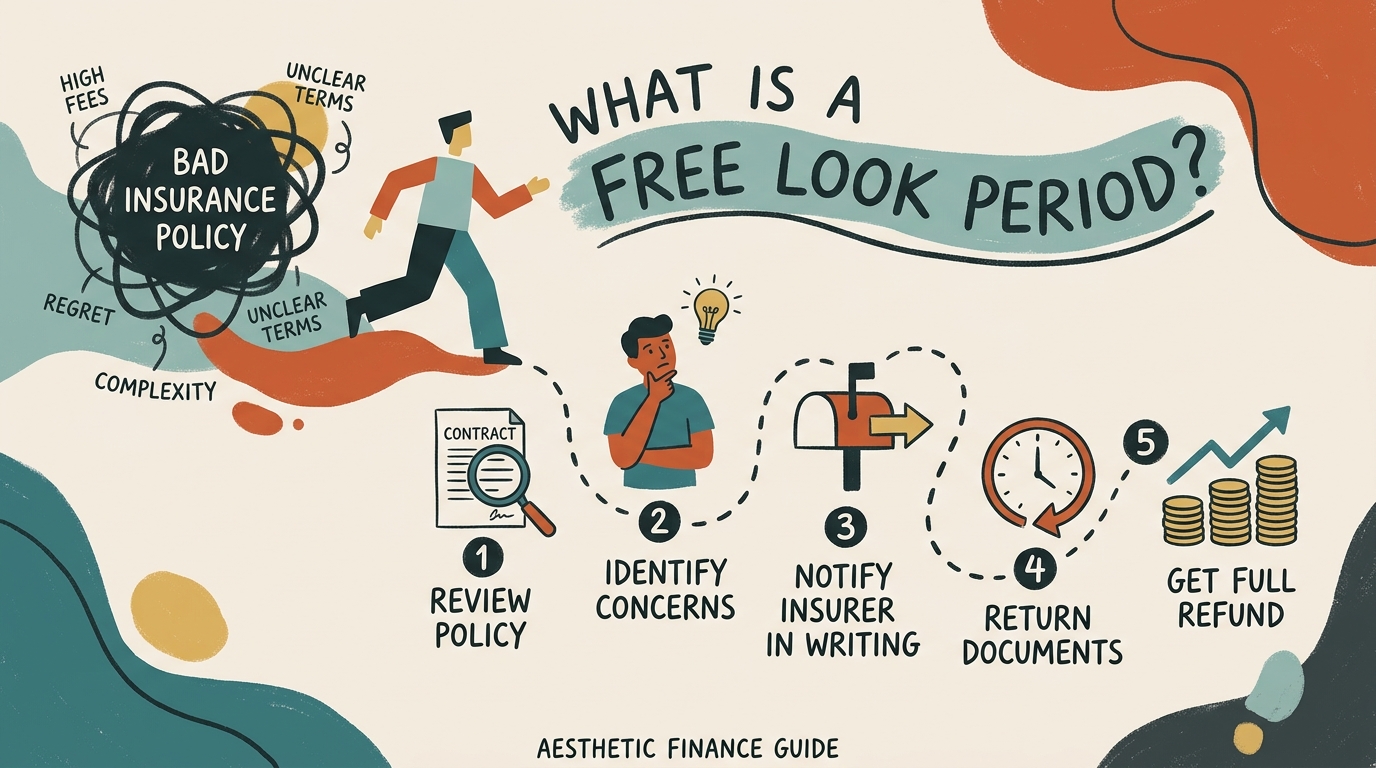

Understanding the Basics of the Free Look Period

The free look period is a mandatory provision enforced by the Reserve Bank of India and the IRDAI. It grants policyholders a specific timeframe to examine the policy document thoroughly. If you find discrepancies, you have the right to return the policy for a refund.

This period is designed to protect consumers from aggressive sales tactics. Whether you bought life insurance or health insurance, knowing what is a free look period empowers you to take control of your money management decisions.

1. The Standard 15-Day Window for Policy Review

Most insurance policies in India come with a standard 15-day free look period. This countdown begins the moment you receive your physical or digital policy bond. It is not tied to the date you paid your premium.

During these 15 days, read the policy document carefully. Check the sum assured, the premium payment term, and the exclusions. If you discover that the features promised by the agent do not match the document, you should initiate the cancellation process immediately.

2. How to Initiate the Cancellation Process

If you have decided that the policy is not right for you, you must act fast. To exercise your right, you need to submit a written request to the insurance company. Clearly state that you are invoking the free look period to cancel the policy.

Ensure you attach a copy of the policy bond and a cancelled cheque for the refund. Sending this request via email or registered post is recommended to maintain a paper trail. Do not rely solely on verbal communication with your agent.

3. Understanding the Refund Calculation

Many people ask what is a free look period regarding the money they get back. You are entitled to a refund of the premium paid, minus certain deductions. These deductions typically include stamp duty charges and medical examination costs incurred by the insurer.

For example, if you paid a premium of ₹50,000, the insurer might deduct ₹500 for medical tests and stamp duty. You will receive the remaining ₹49,500 back in your bank account. This is a small price to pay for exiting a policy that does not serve your financial goals.

4. Why Agents Might Discourage You

Insurance agents often receive high commissions for selling policies. If you cancel during the free look period, the agent loses their commission. Consequently, they may try to convince you that the policy is perfect for you or that cancelling is a complicated process.

Do not be swayed by these tactics. You are the customer, and you have the legal right to cancel. If an agent tricked you into buying a policy you cannot afford or do not need, the free look period is your best tool for rectification.

5. Essential Documents You Need to Keep

To successfully cancel a policy, documentation is key. Keep a copy of the original proposal form and the welcome letter sent by the insurer. These documents prove when you received the policy, which is vital for calculating the 15-day window.

If you are unsure about what is a free look period in your specific contract, check the policy schedule. It is mandatory for insurers to mention this clause in the document. If it is missing, you may have grounds to complain to the insurance ombudsman.

Ultimately, the free look period is a vital consumer right. It prevents financial loss and ensures transparency in the insurance sector. Always review your documents within the stipulated time to protect your hard-earned money.