Choosing between a fixed vs floating rate home loan is perhaps the most significant decision a borrower makes when financing a dream home. With property prices rising, understanding how your interest rate behaves over a 20-year tenure is essential for long-term financial stability.

At money management, we believe that informed borrowers make better decisions. Whether you are a first-time buyer or looking to refinance, knowing the mechanics of these two interest structures can save you lakhs of rupees in interest payments.

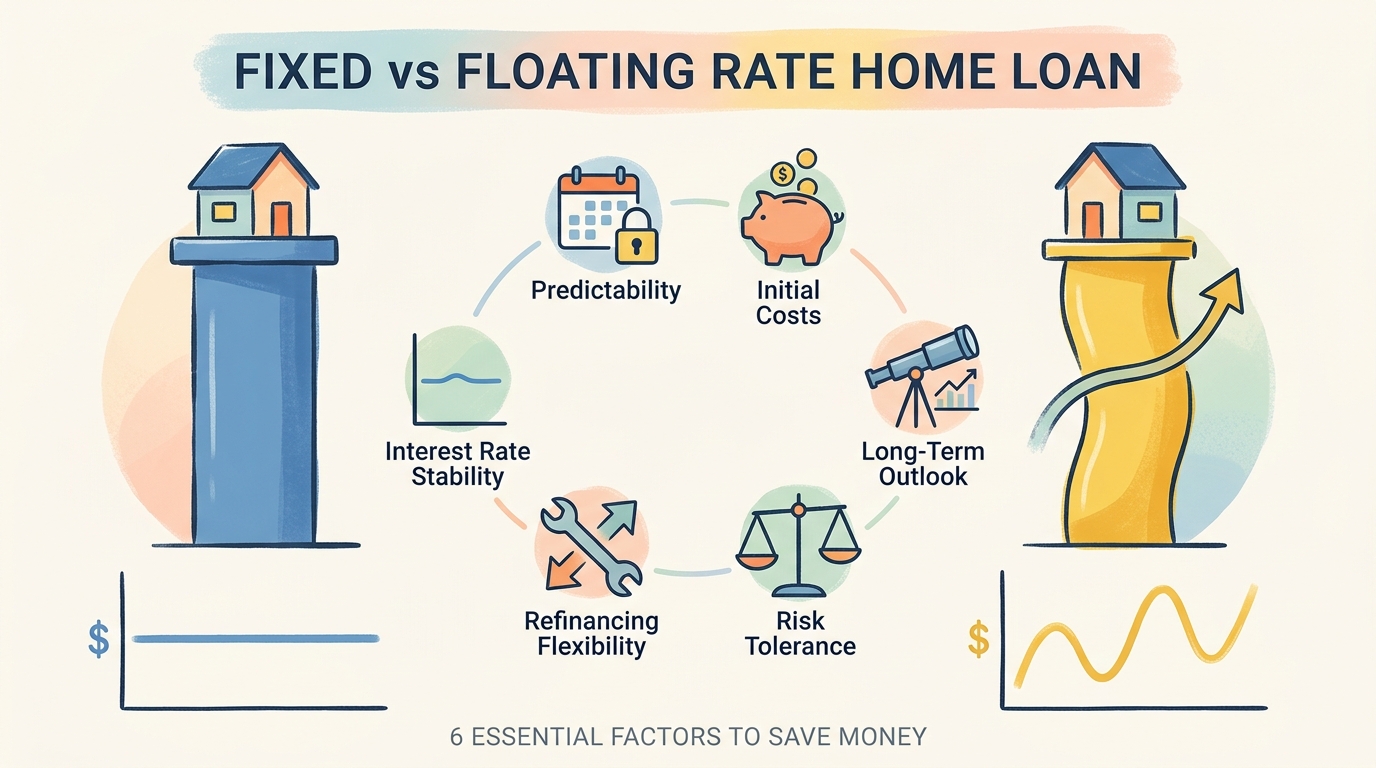

Understanding the Core Differences

A fixed vs floating rate home loan comparison begins with how the interest is calculated. A fixed rate remains constant throughout the tenure, regardless of market fluctuations. Conversely, a floating rate is linked to an external benchmark, such as the repo rate set by the Reserve Bank of India.

1. Predictability with Fixed Rate Home Loans

Fixed rate loans offer peace of mind. Your EMI remains unchanged even if the economy experiences high inflation or interest rate hikes. This is ideal for individuals on a strict monthly budget who cannot afford sudden increases in their financial obligations.

However, lenders often charge a premium for this certainty. You might start with an interest rate that is 1% to 2% higher than current floating rates. Over a 20-year period, this difference can lead to paying significantly more in total interest.

2. The Flexibility of Floating Rate Home Loans

Floating rate loans are the most popular choice in India. These rates are dynamic and adjust based on the lender’s benchmark. When the central bank reduces rates, your interest burden decreases automatically, often leading to a shorter loan tenure.

While this offers the potential for lower long-term costs, it introduces volatility. If interest rates spike due to global economic conditions, your EMI or tenure will increase. You must maintain a financial buffer to handle these unexpected surges.

3. Why Floating Rates Often Win the Economic Wave

When analyzing a fixed vs floating rate home loan, historical data suggests that floating rates are generally more economical. Economic cycles tend to move in waves; while rates rise, they also fall. Over a long tenure, these dips often compensate for the peaks.

Fixed rates are essentially a bet against the market. By choosing a fixed rate, you are paying a premium to protect yourself from future rate hikes. Unless you are certain that interest rates will skyrocket, the floating rate usually proves to be the cheaper option.

4. Evaluating Your Risk Appetite

Your choice should align with your personal risk tolerance. If you have a stable income and a high debt-to-income ratio, a fixed rate might provide the security you need to avoid default. If you have surplus funds and can handle EMI fluctuations, a floating rate is mathematically superior.

Always calculate the total cost of credit before signing the agreement. A fixed vs floating rate home loan decision is not just about the current rate; it is about the total interest paid over the entire duration of the loan.

5. Prepayment and Refinancing Options

Many borrowers overlook the importance of prepayment. Floating rate loans in India typically do not attract prepayment penalties for individual borrowers. This allows you to pay off your principal faster when you have extra cash, further reducing your interest liability.

Fixed rate loans may have stricter terms regarding prepayment. If you decide to switch your loan to a different lender to get a better rate, you might face significant exit fees. Always check the fine print regarding fixed vs floating rate home loan exit clauses.

6. Impact of Economic Indicators

The fixed vs floating rate home loan debate is heavily influenced by macroeconomic factors. When inflation is high, the central bank increases the repo rate, which pushes up floating rates. Conversely, during economic slowdowns, rates are slashed to encourage borrowing.

By staying updated with financial news, you can time your loan application. If you expect rates to fall, a floating rate is a strategic choice. If you anticipate a period of prolonged instability, locking in a rate might be a defensive, albeit costlier, strategy.

Ultimately, the fixed vs floating rate home loan choice depends on your financial goals. Most experts recommend floating rates for their transparency and cost-efficiency. However, if you value absolute EMI stability above all else, a fixed rate remains a viable, if expensive, alternative.

Before finalizing your home loan, compare the fixed vs floating rate home loan offers from multiple banks. Use online calculators to see how a 0.5% difference in interest can impact your total repayment. Choosing the right fixed vs floating rate home loan structure is the first step toward successful home ownership.

Remember, the fixed vs floating rate home loan decision is not permanent. Many lenders allow you to convert your floating rate to fixed or vice versa for a nominal fee. Stay flexible, keep an eye on the market, and manage your debt wisely.