Understanding the nuances of LTCG vs STCG tax india is essential for every investor looking to build long-term wealth. The Indian tax system is designed to encourage patient investing, rewarding those who hold assets for extended periods with significantly lower tax rates.

When you sell an asset like stocks, mutual funds, or real estate for a profit, the government views this gain as income. However, the tax treatment depends entirely on how long you held that asset before selling. Mastering LTCG vs STCG tax india can save you thousands of rupees annually.

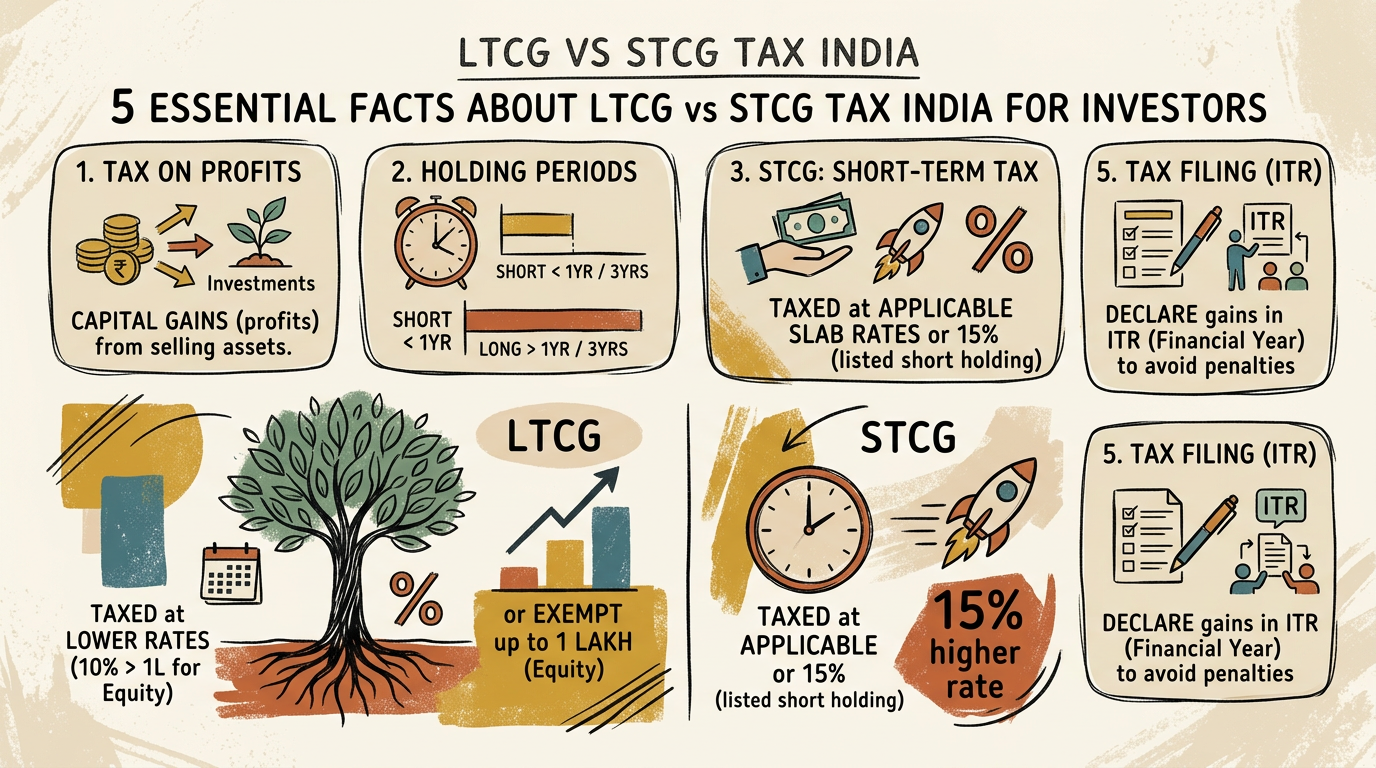

Understanding Capital Gains in India

Capital gains are the profits you make from selling a capital asset. To calculate these, you subtract the cost of acquisition and any transfer expenses from the final sale price. The Reserve Bank of India provides the regulatory framework that supports our financial markets, but the Income Tax Department dictates how these gains are taxed.

Whether you are a day trader or a long-term investor, your tax liability hinges on the classification of your gains. If you want to master your overall money management, you must understand how these tax slabs impact your net returns.

1. Defining Short-Term Capital Gains (STCG)

STCG occurs when you sell an asset within a specific short duration. For listed equity shares and equity-oriented mutual funds, the holding period is less than 12 months. For other assets like debt funds or physical gold, the threshold is typically 36 months.

STCG is generally taxed at a higher rate because the government discourages speculative, short-term trading. For equity, STCG is taxed at a flat rate of 15% plus applicable cess. This is a crucial point in the LTCG vs STCG tax india debate, as it often eats into the profits of active traders.

2. Defining Long-Term Capital Gains (LTCG)

LTCG is the profit earned from assets held for a longer duration. For equity, this is anything beyond 12 months. Because the government wants to promote capital formation and stable markets, they offer preferential tax treatment for long-term investments.

Currently, LTCG on equity above ₹1.25 lakh in a financial year is taxed at 12.5%. This lower rate is the primary reason why financial advisors emphasize the “buy and hold” strategy. When analyzing LTCG vs STCG tax india, the tax efficiency of long-term holding becomes clear.

3. The Impact of Holding Periods on Tax Liability

The difference in tax rates is significant. If you sell a stock after 11 months, you pay 15% on the entire gain. If you hold that same stock for 13 months, you benefit from the lower 12.5% rate and the ₹1.25 lakh exemption limit.

Investors often overlook the power of compounding combined with tax efficiency. By holding assets longer, you not only benefit from market growth but also from the government’s incentive structure. This is why understanding LTCG vs STCG tax india is a cornerstone of smart financial planning.

4. Tax Exemptions and Indexation Benefits

For non-equity assets like real estate or gold, the rules for LTCG vs STCG tax india are different. LTCG on these assets often allows for “indexation.” Indexation adjusts the purchase price of an asset for inflation, effectively reducing your taxable profit.

While equity investments don’t get indexation, they enjoy the lower 12.5% rate. Always keep your purchase documents safe, as they are required to calculate your cost of acquisition accurately. Proper record-keeping is vital for tax compliance.

5. Strategic Planning for Tax Optimization

To optimize your tax, consider the timing of your sales. If you are close to the 12-month mark, waiting a few extra days could shift your tax liability from STCG to LTCG. This simple move can drastically improve your post-tax returns.

Furthermore, utilize the ₹1.25 lakh LTCG exemption limit effectively. Some investors practice “tax-loss harvesting,” where they sell losing stocks to offset gains, though this requires careful calculation. Ultimately, the LTCG vs STCG tax india framework rewards those who plan their exits with the same care they use to choose their investments.

Conclusion

Navigating the complexities of LTCG vs STCG tax india does not have to be intimidating. By understanding the holding periods and the associated tax rates, you can make informed decisions that protect your capital.

Remember, the goal is to maximize your wealth while remaining compliant with tax laws. Whether you are dealing with equity or other assets, keeping these rules in mind will ensure you keep more of your hard-earned money. Always consult with a tax professional to tailor these strategies to your specific financial situation.