When planning your financial future, choosing the right tax-saving instrument is crucial. The debate of ELSS vs PPF often confuses investors looking to optimize their Section 80C deductions. Both serve different purposes, risk appetites, and financial goals.

Understanding the nuances of these two popular investment avenues is essential for effective money management. While one offers government-backed security, the other leverages the growth potential of the equity markets.

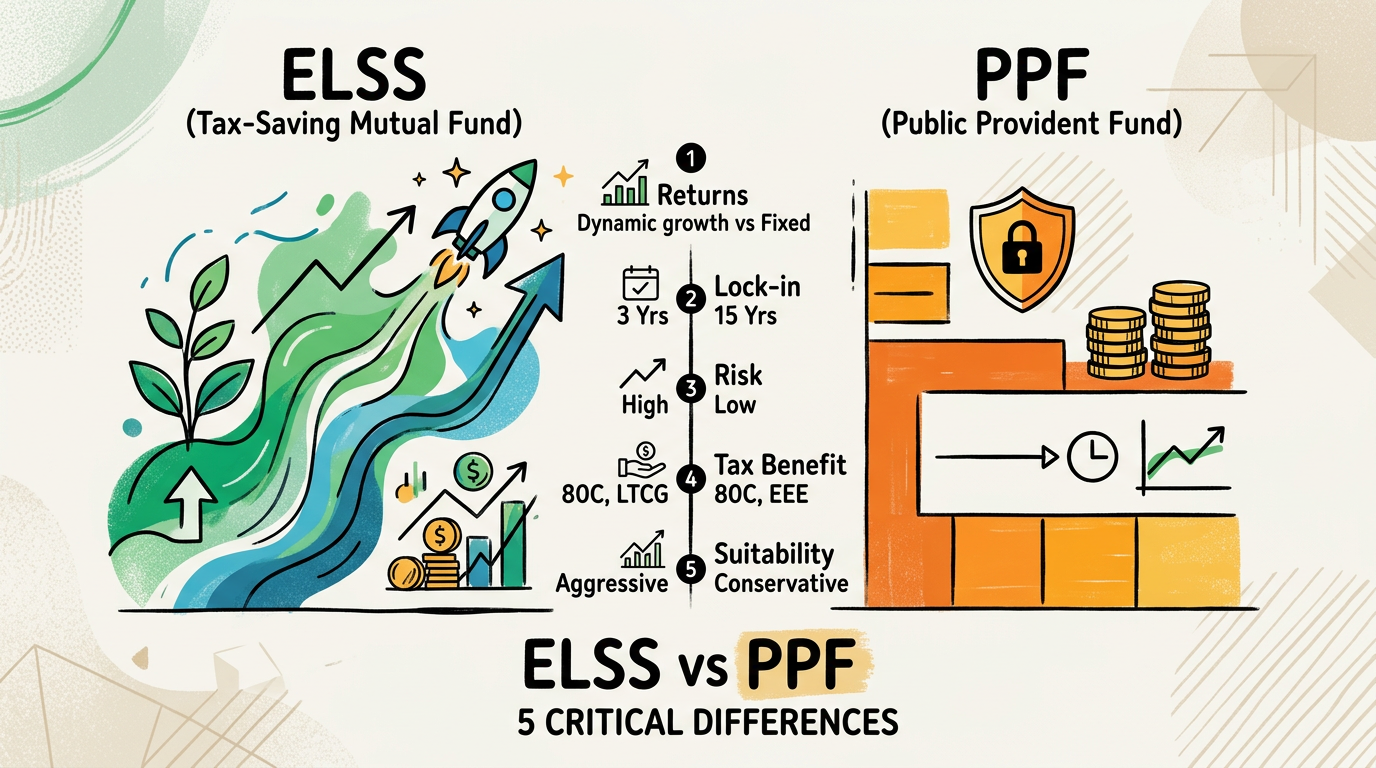

Understanding the Core Differences

To make an informed decision regarding ELSS vs PPF, you must analyze their underlying structures. ELSS, or Equity Linked Savings Schemes, are mutual funds that invest primarily in equities. In contrast, the Public Provident Fund (PPF) is a long-term debt instrument backed by the government.

The Reserve Bank of India provides the regulatory framework that ensures the safety of debt-based schemes like PPF. ELSS, however, is regulated by SEBI and is subject to market risks. Let us dive into the 5 key factors that define this showdown.

1. Lock-in Period Comparison

The lock-in period is a major differentiator in the ELSS vs PPF battle. ELSS has the shortest lock-in period among all Section 80C investments, set at just 3 years. This allows for better liquidity if you need your funds back sooner.

PPF, on the other hand, comes with a mandatory 15-year lock-in period. While partial withdrawals are allowed after 7 years, the funds remain largely inaccessible for a long duration. If you prioritize liquidity, ELSS is the clear winner.

2. Risk and Return Potential

When comparing ELSS vs PPF, you are essentially choosing between volatility and stability. ELSS investments are exposed to market fluctuations, which can lead to higher returns over the long term. Historically, equity markets have outperformed debt instruments significantly.

PPF offers fixed, government-guaranteed interest rates, making it a safe haven for risk-averse investors. While it won’t make you wealthy overnight, it protects your capital from market crashes. It is the tortoise of the investment world, moving slowly but surely.

3. Taxation of Gains

Taxation is a vital component of the ELSS vs PPF analysis. ELSS gains are treated as Long Term Capital Gains (LTCG). Gains exceeding ₹1.25 lakh in a financial year are taxed at 12.5%.

PPF is an EEE (Exempt-Exempt-Exempt) instrument. The investment, the interest earned, and the maturity amount are all completely tax-free. This makes PPF highly attractive for those in higher tax brackets looking for guaranteed tax-free income.

4. Investment Flexibility

ELSS allows you to start an investment with as little as ₹500 through a Systematic Investment Plan (SIP). This flexibility makes it accessible for young professionals starting their investment journey.

PPF requires a minimum annual investment of ₹500 and a maximum of ₹1.5 lakh per financial year. You cannot invest more than the limit, which restricts the potential for aggressive wealth accumulation through this single channel.

5. Suitability for Financial Goals

Choosing between ELSS vs PPF depends on your life stage. If you are young and have a long horizon, the wealth-creation potential of ELSS is superior. It helps beat inflation, which is necessary for long-term goals like retirement or house purchases.

PPF is ideal for those nearing retirement or those who cannot afford to lose any portion of their principal. It provides a reliable cushion that complements your overall portfolio. A balanced investor often holds both to mitigate risk while seeking growth.

Final Verdict on ELSS vs PPF

The ELSS vs PPF comparison ultimately boils down to your personal financial objectives. If you seek growth and can tolerate market volatility, ELSS is your best bet. If you prioritize safety and tax-free returns, PPF remains the gold standard.

Many successful investors utilize ELSS vs PPF strategically by splitting their Section 80C allocation between both. This hybrid approach provides the perfect blend of safety and aggressive growth. Always assess your risk profile before committing your hard-earned money to either instrument.