Many taxpayers believe that transferring assets to a non-earning spouse is a clever way to reduce their tax liability. However, the Income Tax Act has specific provisions to prevent such tax evasion. Understanding clubbing of income explained is essential for every investor in India.

When you transfer money or assets to your spouse without adequate consideration, the tax authorities do not ignore it. Instead, they apply the clubbing provisions, which effectively nullify the tax benefit you hoped to achieve. You must master money management to ensure your financial planning remains compliant with the law.

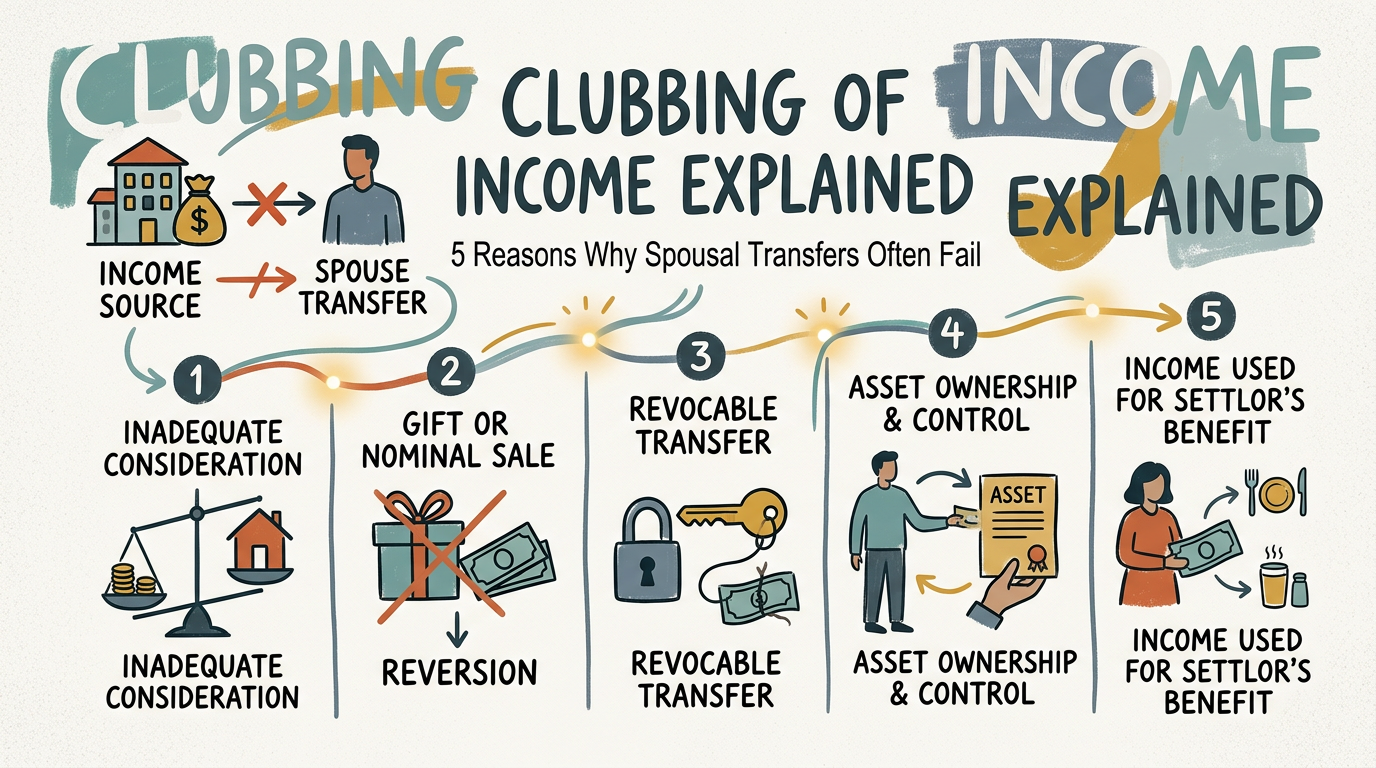

The Reality of Tax Planning Through Spouses

It is a common misconception that gifting money to a spouse creates a separate tax entity. While it is legal to gift money, the income generated from that money is often treated as your own. If you fail to account for this, you may face scrutiny from the Income Tax Department.

The concept of clubbing of income explained ensures that individuals cannot shift their tax burden to a spouse in a lower tax bracket. If you transfer ₹5,00,000 to your spouse to invest, the interest earned will be added to your taxable income. This defeats the entire purpose of the strategy.

1. Direct Transfers Without Consideration

If you transfer funds to your spouse as a gift, the income generated from those funds is clubbed with your income. For instance, if you gift ₹10,00,000 and it earns ₹70,000 in interest, that ₹70,000 is added to your total income. You must report this correctly to avoid penalties.

2. Indirect Transfers and Circular Transactions

Some taxpayers attempt to bypass rules through circular transfers, such as gifting money to a relative who then gifts it to the spouse. The law is designed to see through these arrangements. The authorities look at the substance of the transaction, not just the form.

3. Assets Transferred Before Marriage

If you transfer assets before marriage, the clubbing provisions generally do not apply to the income generated from those assets after marriage. However, once you are married, any transfer of assets for inadequate consideration triggers the clubbing rules.

4. Income from Re-invested Income

The law states that if the income earned from the gifted asset is further invested, the income from that second investment is not clubbed. This is a subtle nuance where clubbing of income explained becomes complex. However, the initial income remains taxable in your hands.

5. Assets Transferred for Adequate Consideration

If you sell an asset to your spouse at fair market value, the clubbing provisions do not apply. You must ensure that the transaction is documented properly. This is a legitimate way to structure your finances without violating tax laws.

Why You Should Avoid Aggressive Tax Planning

Attempting to bypass tax laws can lead to significant financial penalties and legal stress. It is far better to focus on legitimate tax-saving instruments like ELSS, PPF, or NPS. Relying on clubbing of income explained as a loophole is a dangerous game that rarely pays off in the long run.

Always maintain clear records of all financial transactions between family members. If you are unsure about a specific transaction, consult a qualified Chartered Accountant. Proper documentation is your best defense against tax audits.

Conclusion

Understanding clubbing of income explained is a fundamental part of responsible financial planning in India. By attempting to shift income to a spouse, you are likely creating more work for yourself during tax filing season. Focus on transparent and legal methods to optimize your tax liability.

Remember, the goal of tax planning is to pay what is legally due, not to evade taxes through complex schemes. Keep your finances clean, stay informed, and always prioritize compliance. For more insights on clubbing of income explained, continue following our expert guides.

Ultimately, the clubbing of income explained clearly shows that the Income Tax Act is designed to prevent revenue leakage. Do not let the allure of tax savings lead you into a trap. Stay compliant and keep your financial future secure.

Final note: Always verify the latest updates on clubbing of income explained with the official government portals. Tax laws are subject to change, and staying updated is the hallmark of a smart investor.