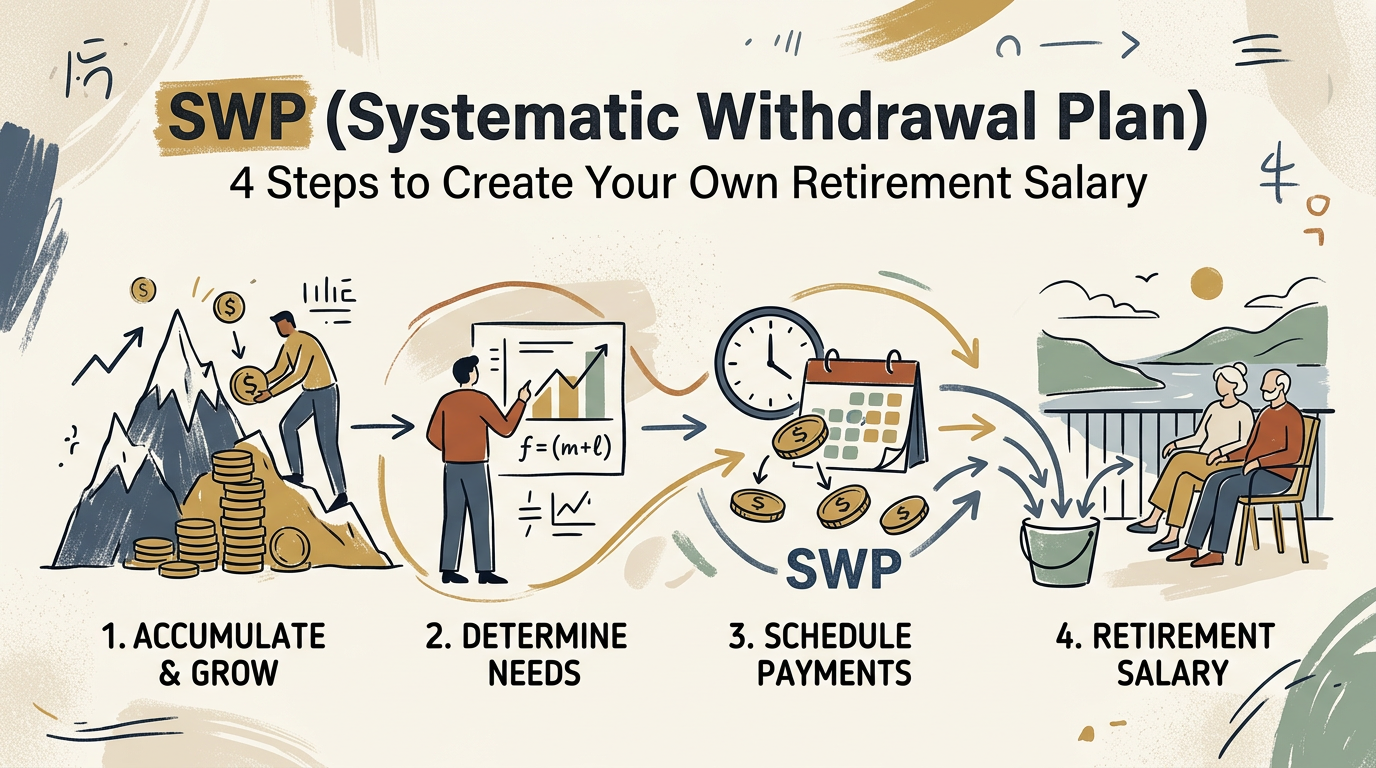

Retirement planning is often focused on the accumulation phase, but the true test of financial freedom lies in the distribution phase. If you have spent years building a corpus, you need a reliable mechanism to convert those assets into a steady stream of income. This is where a SWP (Systematic Withdrawal Plan) becomes an essential tool for every retiree.

Think of a SWP (Systematic Withdrawal Plan) as the exact mirror image of a SIP. While a SIP helps you build wealth by investing small amounts regularly, a SWP (Systematic Withdrawal Plan) helps you consume that wealth by withdrawing fixed amounts at regular intervals. It is effectively creating your own personal salary from your investments.

For those looking to master the art of money management, understanding how to structure your withdrawals is just as important as understanding how to save. Let us explore how you can leverage this strategy to secure your post-retirement life.

Understanding the Mechanics of SWP

A SWP (Systematic Withdrawal Plan) allows investors to withdraw a fixed sum of money from their mutual fund investments at predetermined intervals—monthly, quarterly, or annually. The remaining balance stays invested in the fund, continuing to grow based on market performance.

This strategy provides a tax-efficient way to generate cash flow. Unlike dividends, which are subject to specific tax rules, a SWP (Systematic Withdrawal Plan) allows you to withdraw only the capital gains or a mix of capital and gains, which can be more favorable depending on your tax slab.

1. How to Calculate Your Monthly Retirement Salary

The first step in setting up a SWP (Systematic Withdrawal Plan) is determining how much you actually need. You must account for inflation, as the purchasing power of ₹50,000 today will not be the same in twenty years.

Start by listing your essential expenses, such as housing, healthcare, and groceries. Once you have a total, ensure your corpus is large enough to sustain these withdrawals without depleting the principal too quickly. You can consult the Reserve Bank of India guidelines on inflation to better understand long-term economic trends.

2. Choosing the Right Mutual Fund Category

Not all funds are suitable for a SWP (Systematic Withdrawal Plan). You generally want funds that offer a balance between growth and stability. Debt funds or hybrid funds are often preferred by retirees because they are less volatile than pure equity funds.

By choosing a fund with moderate risk, you ensure that your principal remains relatively safe while still earning returns that beat inflation. Always review the expense ratio and the historical performance of the fund before committing your retirement corpus.

3. Tax Efficiency and Capital Gains

One of the biggest advantages of a SWP (Systematic Withdrawal Plan) is its tax efficiency. When you withdraw money, you are only taxed on the capital gains portion of the redemption, not the entire withdrawal amount.

This is significantly better than receiving dividends, which are added to your total income and taxed at your applicable slab rate. For long-term capital gains on equity-oriented funds, you only pay tax on gains exceeding ₹1.25 lakh, making this a highly attractive option for retirees.

4. The Importance of Staying Invested

The beauty of a SWP (Systematic Withdrawal Plan) is that your money does not sit idle. Even as you withdraw your monthly “salary,” the remaining units in your mutual fund continue to participate in market growth.

If the market performs well, your corpus might even grow despite your withdrawals. This creates a sustainable cycle where your investments work for you, providing a reliable income stream while preserving your wealth for the long term.

In conclusion, a SWP (Systematic Withdrawal Plan) is the ultimate retirement companion. By planning your withdrawals carefully and selecting the right funds, you can enjoy your golden years with financial independence and peace of mind.