In the world of personal finance, choosing the right insurance product is a critical decision that impacts your family’s future. Many investors find themselves caught in the ULIP vs term insurance debate, often swayed by aggressive marketing tactics.

Insurance companies love to sell products that promise the world. They frame these policies as all-in-one solutions, much like a shampoo and conditioner combo. However, just as those products often fail to provide the deep conditioning of a dedicated treatment, hybrid financial products often underperform.

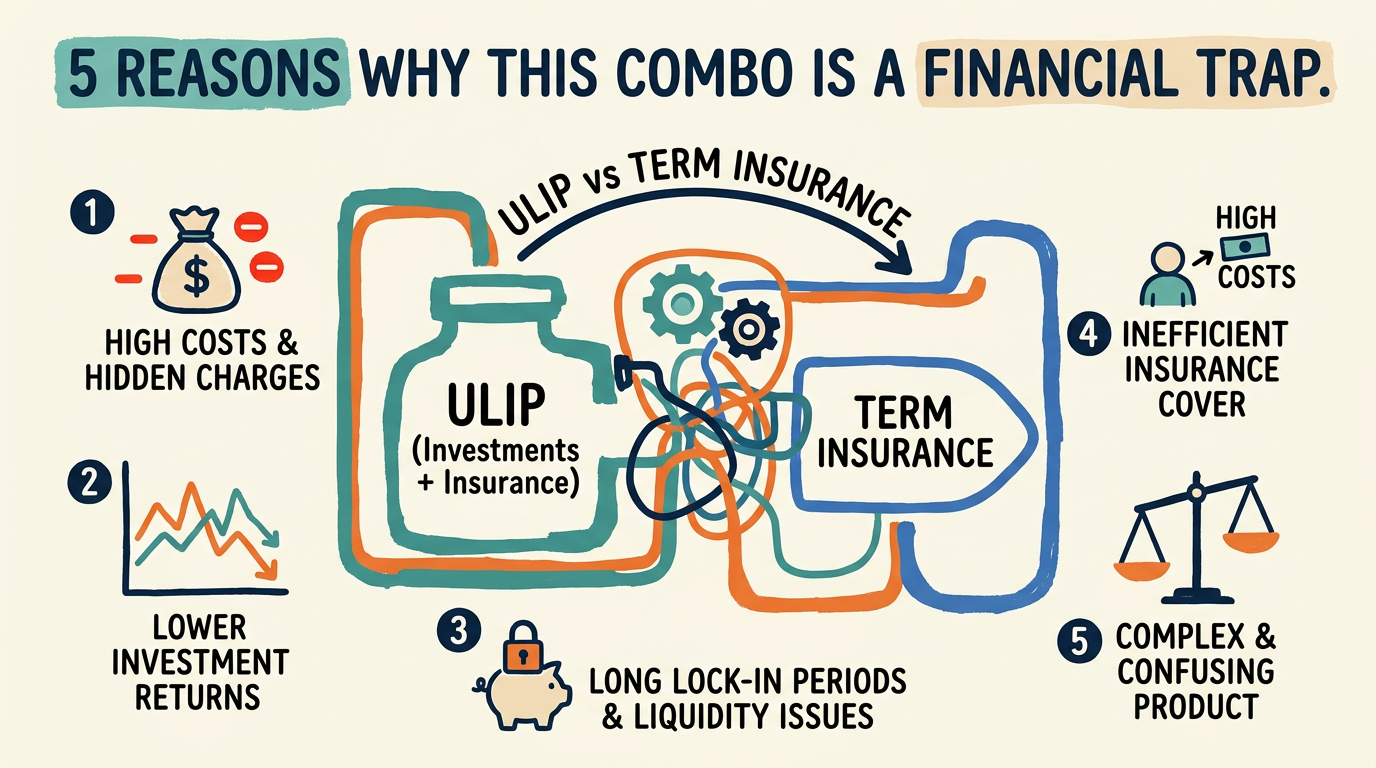

Understanding the core differences between these two is essential for effective money management. Let us break down why this comparison is the ultimate trap for the average investor.

The Illusion of the All-in-One Policy

A Unit Linked Insurance Plan (ULIP) attempts to combine life cover with market-linked investment returns. On the surface, this sounds convenient. You pay one premium, and you get both protection and wealth creation.

However, the reality is that by trying to do both, ULIPs often fail to do either well. High administrative charges and mortality costs eat into your potential returns. When you analyze ULIP vs term insurance, you realize that separating these two goals is almost always the superior financial strategy.

1. Why Term Insurance is the Gold Standard for Protection

Term insurance is the purest form of life cover. You pay a small premium, and in exchange, the insurer promises a large sum assured to your family if something happens to you.

It is designed for one purpose: protection. Because there is no investment component, the premiums are incredibly affordable. For a cover of ₹1 Crore, a healthy individual might pay as little as ₹10,000 to ₹15,000 annually.

This efficiency allows you to secure your family’s future without breaking the bank. It is the foundation of any robust financial plan, as recommended by the Reserve Bank of India guidelines on financial literacy.

2. The Hidden Costs That Make ULIPs a Trap

When you look at ULIP vs term insurance, you must look at the cost structure. ULIPs come with a basket of charges, including premium allocation charges, policy administration charges, and fund management fees.

These charges are deducted from your premium before it is even invested. Over a 10 or 15-year period, these costs significantly erode the power of compounding. You might find that your actual investment corpus is much lower than what you would have achieved by investing in a low-cost index fund.

Furthermore, the life cover provided by a ULIP is often insufficient. If you are paying ₹50,000 annually for a ULIP, you might only get a cover of ₹5 Lakhs. This is nowhere near enough to sustain a family in the event of a tragedy.

3. The Flexibility of Separating Insurance and Investment

The smartest way to handle your finances is to decouple your protection and your growth. By choosing term insurance for protection, you pay a minimal amount for a high sum assured.

With the money you save by not buying a high-cost ULIP, you can invest in diversified mutual funds or public provident funds. This gives you full control over your investment strategy and risk profile.

When you compare ULIP vs term insurance, the flexibility of the “buy term and invest the difference” strategy is unmatched. You are not locked into a rigid product that charges you for the privilege of underperforming.

4. Tax Implications and Liquidity Concerns

Both products offer tax benefits under Section 80C of the Income Tax Act. However, ULIPs often have a mandatory lock-in period of five years, during which your money is inaccessible.

In contrast, when you invest the difference in mutual funds, you have much higher liquidity. You can access your funds during emergencies, which is a vital aspect of sound financial planning.

The ULIP vs term insurance debate often ignores this liquidity factor. Being locked into a poor-performing investment just for the sake of a tax deduction is a common mistake that many retail investors make.

5. Evaluating the True Cost of Convenience

The convenience of a single premium payment is the primary marketing hook for ULIPs. But is that convenience worth the cost of lower returns and inadequate protection?

Most financial experts agree that it is not. When you evaluate ULIP vs term insurance, you should prioritize the efficiency of your capital. You want your protection to be cheap and your investments to be high-growth.

By keeping these two functions separate, you avoid the “shampoo + conditioner” trap. You get the best-in-class protection of term insurance and the market-beating potential of dedicated investment vehicles.

Final Verdict: Don’t Fall for the Trap

The ULIP vs term insurance comparison is clear once you strip away the marketing jargon. Term insurance is a necessity for anyone with dependents, while ULIPs are often expensive, inefficient investment products.

Do not let the promise of an all-in-one policy cloud your judgment. Focus on securing your family with a high-cover term plan and building your wealth through disciplined, low-cost investments. Understanding the ULIP vs term insurance dynamic is the first step toward true financial independence.

Ultimately, your money deserves better than a product that tries to do everything and succeeds at nothing. Choose the path of clarity, lower costs, and better outcomes for your family’s future.