Navigating the complexities of medical coverage can be daunting, especially when you are already dealing with a health crisis. Understanding the fundamental differences between cashless vs reimbursement health insurance is essential for every policyholder in India.

When you are admitted to a hospital, the last thing you want to worry about is managing a massive financial burden. Choosing the right claim settlement process can significantly impact your stress levels and your bank balance.

Whether you are looking for money management tips or trying to secure your family’s future, knowing how these two systems function is the first step toward financial stability.

Understanding the Basics of Health Insurance Claims

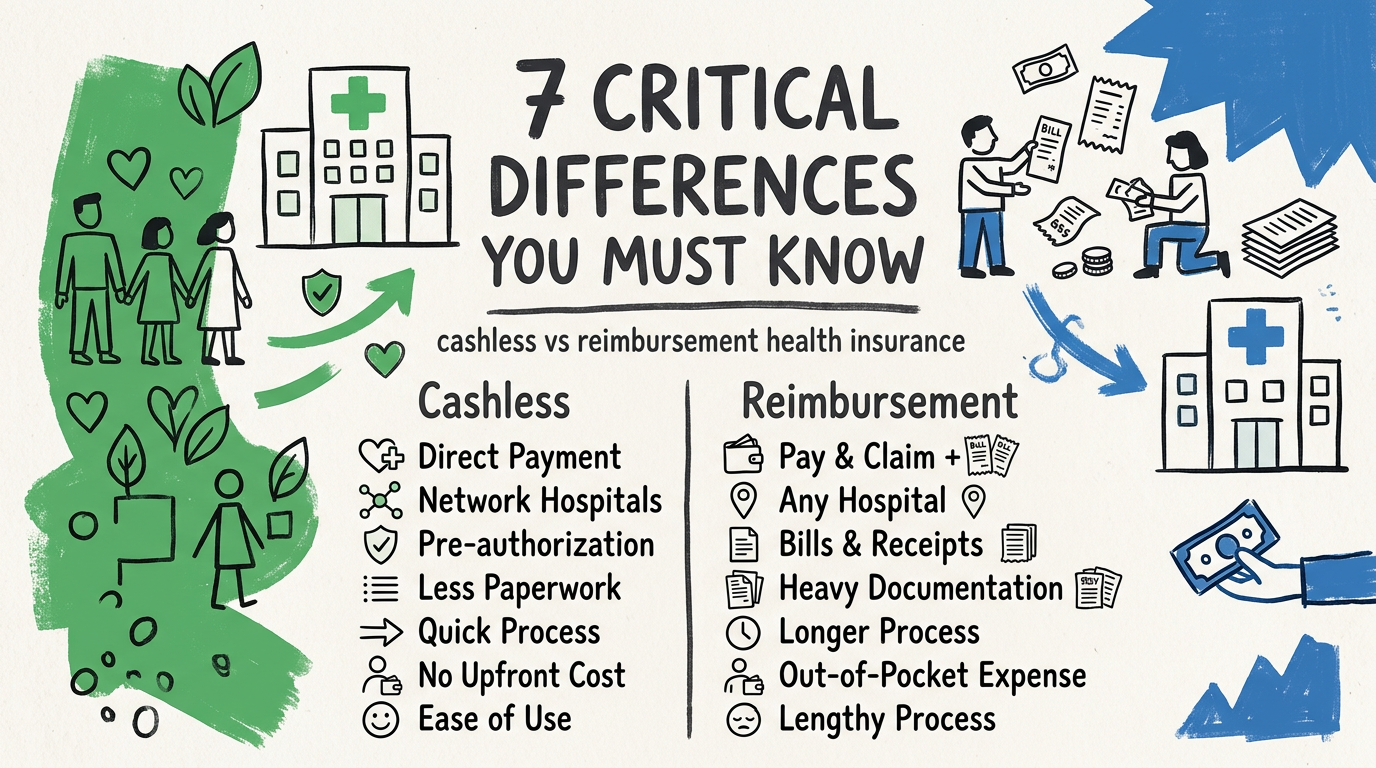

In the Indian insurance landscape, there are two primary ways to settle medical bills. One allows you to walk out of the hospital without paying a single rupee, while the other requires you to pay upfront and claim the money back later.

If you want to master your personal finances, you must understand how these mechanisms work. Let’s break down the 7 key factors that define the cashless vs reimbursement health insurance debate.

1. The Convenience of Cashless Hospitalization

A cashless facility is the gold standard for medical emergencies. Under this system, the insurance company settles the bill directly with the hospital network.

You only need to provide your health card and identity proof at the hospital’s TPA desk. This eliminates the need for arranging large sums of cash during a crisis.

It is important to note that this facility is only available at network hospitals. You can check the list of these hospitals on the Insurance Regulatory and Development Authority of India portal.

2. The Reality of Reimbursement Claims

Reimbursement is the traditional method where you pay the hospital bills out of your own pocket. Once discharged, you submit all original bills, prescriptions, and reports to the insurer.

The insurance company then reviews your documents and transfers the approved amount to your bank account. This process can take anywhere from 15 to 30 days.

This method is often necessary if you choose to get treated at a non-network hospital. It requires meticulous record-keeping and patience.

3. Financial Impact on Your Savings

The cashless vs reimbursement health insurance choice has a direct impact on your liquidity. With cashless, your savings remain untouched, allowing you to focus entirely on recovery.

Conversely, reimbursement requires you to have a significant emergency fund ready. If a surgery costs ₹5,00,000, you must have that amount available immediately to pay the hospital.

For many families, arranging ₹5,00,000 at short notice can lead to high-interest personal loans. This is why cashless is generally preferred for planned and emergency surgeries.

4. Documentation Requirements

Cashless claims involve a streamlined documentation process handled primarily by the hospital’s insurance desk. They coordinate with the TPA to get pre-authorization.

Reimbursement claims demand a high level of administrative effort from your side. You must collect every single receipt, pharmacy bill, and doctor’s note.

Missing a single document can lead to claim rejection or partial payment. Therefore, if you opt for reimbursement, keep a dedicated file for all medical paperwork.

5. Speed of Settlement

Speed is the biggest advantage of the cashless system. Because the insurer and the hospital are in direct communication, the approval process is usually faster.

Reimbursement is inherently slower. The insurer must verify every claim against the policy terms, which naturally takes more time.

If you are looking for a seamless experience, always prioritize hospitals that are part of your insurer’s network. This simple step can save you weeks of follow-up calls.

6. Network Hospital Limitations

The biggest drawback of cashless is the restriction to network hospitals. If your preferred doctor is not in the network, you cannot use this facility.

Reimbursement gives you the freedom to choose any hospital in India. This is particularly useful for specialized treatments or if you are in a remote location.

When comparing cashless vs reimbursement health insurance, consider the proximity of network hospitals to your home. Having a high-quality network hospital nearby is a major advantage.

7. Hidden Costs and Deductibles

Even in cashless claims, you might have to pay for non-medical expenses. Items like gloves, masks, and administrative charges are often not covered by insurance.

These expenses can add up to ₹10,000 or more depending on the hospital. Always clarify these exclusions before admission to avoid surprises.

Understanding the cashless vs reimbursement health insurance nuances ensures you are never caught off guard. Whether you choose cashless or reimbursement, always ensure your policy covers your specific needs.

Conclusion: Making the Right Choice

The debate between cashless vs reimbursement health insurance ultimately boils down to convenience versus flexibility. While cashless offers peace of mind, reimbursement offers the freedom to choose your healthcare provider.

Most modern policies provide both options. We recommend prioritizing a policy that has a vast network of cashless hospitals to minimize your out-of-pocket expenses.

Remember, the goal of insurance is to protect your wealth. By understanding cashless vs reimbursement health insurance, you are taking a proactive step toward better financial health.

Always review your policy document annually. If you find yourself constantly using reimbursement, it might be time to switch to a provider with a better network in your area.

Finally, keep your insurance details accessible at all times. Whether you opt for cashless vs reimbursement health insurance, having your documents ready is the key to a smooth claim experience.

Evaluating cashless vs reimbursement health insurance is a vital part of your financial planning journey. Choose wisely to protect your hard-earned money and your health.