When shopping for life insurance, you will inevitably encounter a policy type that promises to return all your paid premiums if you survive the term. This is known as the return of premium term insurance trap. On the surface, it sounds like a “win-win” scenario: you get protection, and if you don’t die, you get your money back.

However, beneath the marketing gloss lies a financial decision that often defies basic logic. In this guide, we will dissect why this product is frequently a poor choice for your money management strategy.

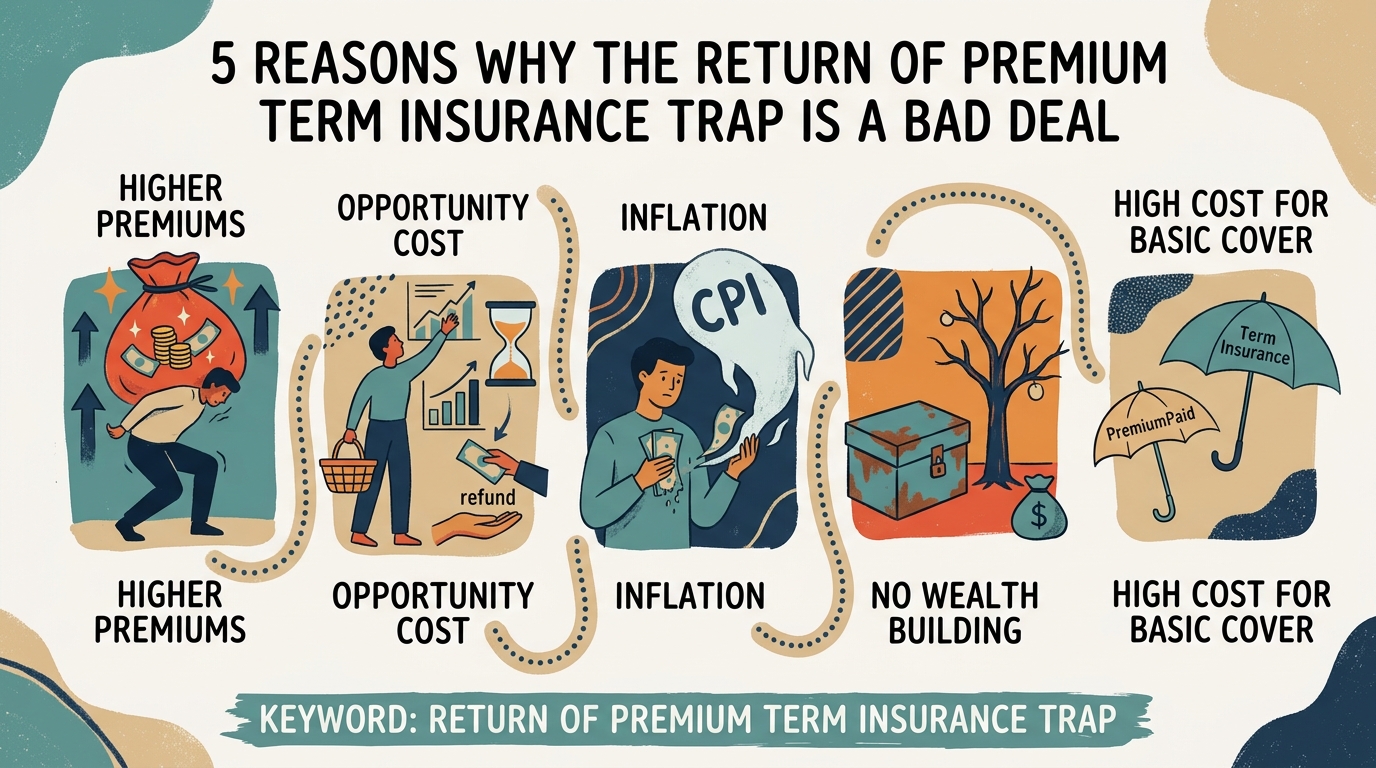

Understanding the Return of Premium Term Insurance Trap

A standard term insurance policy is a pure protection product. You pay a small premium for a large sum assured. If you pass away during the term, your family gets the money. If you survive, the contract expires, and you get nothing back. This is exactly how insurance should work—transferring risk for a fee.

The return of premium term insurance trap changes this dynamic by adding a savings component. Because the insurer must return your premiums at the end of 30 years, they charge you significantly higher premiums upfront. You are essentially paying for the insurance and an additional amount that the insurer invests on your behalf.

1. The Opportunity Cost of Capital

The biggest issue with this policy is the opportunity cost. If you pay ₹15,000 for a standard term plan, you might pay ₹35,000 for a return of premium (ROP) plan. That extra ₹20,000 per year is essentially being locked away for three decades.

If you invested that same ₹20,000 in a diversified equity mutual fund, the compounding effect over 30 years would be substantial. By choosing the return of premium term insurance trap, you lose the ability to grow that money. You are getting back your principal amount in 30 years, but its purchasing power will be decimated by inflation.

2. The Illusion of “Free” Insurance

Marketing materials often claim that ROP plans provide “free” insurance. They argue that since you get your money back, the insurance cost you nothing. This is a dangerous fallacy. You have paid a massive premium for the duration of the policy.

The return of premium term insurance trap relies on the fact that most people do not calculate the time value of money. If you receive ₹10 Lakhs back after 30 years, that amount is worth a fraction of what ₹10 Lakhs is worth today. You are essentially giving the insurance company an interest-free loan for three decades.

3. High Premium Burden

Because the premiums are so much higher, many people end up under-insuring themselves. They might need a cover of ₹2 Crores, but because they want an ROP plan, they settle for ₹1 Crore to keep the premium affordable. This is a critical failure in your financial protection.

Always prioritize the sum assured over the return of premium feature. According to guidelines from the Reserve Bank of India, financial products should be evaluated based on their utility and cost-efficiency. The return of premium term insurance trap fails this test because it forces you to compromise on your family’s security to satisfy a psychological desire to “get something back.”

4. Lack of Flexibility

Life is unpredictable. If you face a financial emergency in year 10, you cannot easily withdraw the money you have “saved” in an ROP policy. Surrendering the policy early often results in a significant loss of the premiums paid.

By falling for the return of premium term insurance trap, you tie your capital to a rigid contract. In contrast, a pure term plan combined with a separate investment portfolio gives you liquidity and control. You can adjust your investments based on market conditions and your personal financial goals.

5. Inflation Erodes the Return

Let’s look at the math. If you pay an extra ₹20,000 annually for 30 years, you have paid ₹6 Lakhs extra. Getting that ₹6 Lakhs back in 2054 is not a gain; it is a loss. Due to inflation, the real value of that money will be significantly lower.

The return of premium term insurance trap ignores the reality of rising costs. You are better off investing that extra money in assets that beat inflation, such as equity or gold. Do not let the promise of a refund distract you from the primary goal of insurance: protecting your family’s standard of living.

Conclusion: Avoid the Return of Premium Term Insurance Trap

The return of premium term insurance trap is a classic example of marketing winning over math. While it feels good to get a refund, the cost of that refund is far higher than the benefit. For your long-term financial health, keep your insurance and your investments separate.

Buy a pure term insurance plan with a high sum assured and invest the difference in low-cost index funds. This strategy provides better protection, higher liquidity, and superior wealth creation. Do not fall for the return of premium term insurance trap; choose logic over the illusion of a refund.