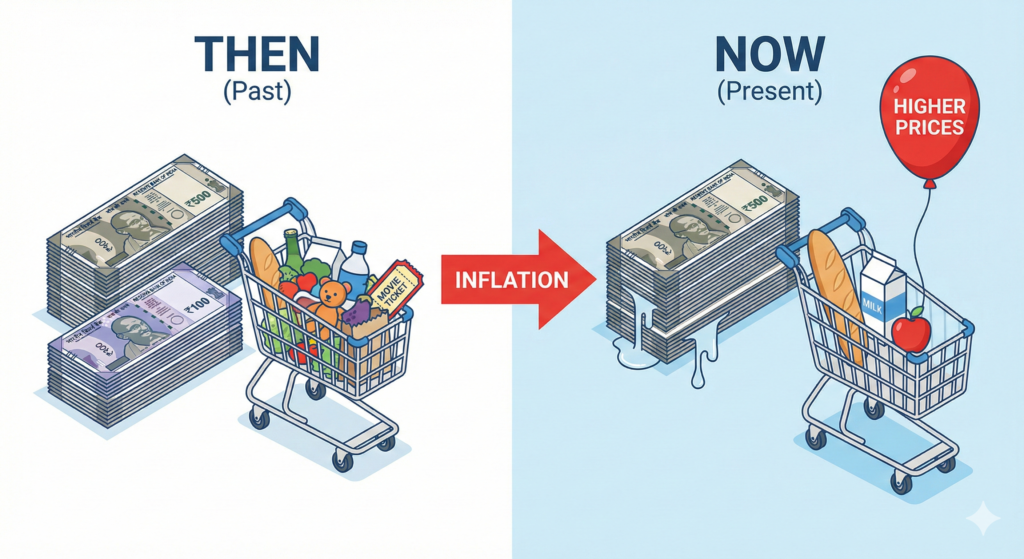

If you have ever wondered what is inflation, just think back to your childhood. Maybe your grandfather gave you ₹100; back then, that note felt like a small fortune. You could buy snacks, a toy, and perhaps even a movie ticket, all while having change left over.

Today? That same ₹100 note barely covers the cost of a premium coffee. You didn’t lose the money, and the note itself hasn’t changed. However, the purchasing power inside that currency has evaporated.

This isn’t bad luck or a random accident. This is inflation. If you don’t understand how it works, it will continue to erode your wealth for the rest of your life.

What Is Inflation? (The Simple Definition)

Economists often define inflation as the rate of increase in prices over a given period. While technically accurate, it is far too clinical. Here is the reality:

Inflation is when your money buys less today than it did yesterday.

Think of it as a slow, invisible leak in your wallet. If inflation sits at 6%—a common figure in India—your ₹1 Lakh savings today will effectively be worth only ₹94,000 in terms of purchasing power next year. You still hold the same amount of cash, but it commands less value in the marketplace.

Why Does It Happen? (The 3 Main Culprits)

In our guide on what is money, we established that currency relies on trust and supply. When that delicate balance shifts, prices rise. There are three primary drivers behind this phenomenon:

1. Demand-Pull Inflation (The “Too Much Money” Problem)

Imagine an auction for a rare item. When ten people compete for one product, the price skyrockets. This is demand-pull inflation. When consumers have excess cash and compete for a limited supply of goods, prices naturally climb. This is a common byproduct of a booming economy.

2. Cost-Push Inflation (The “Expensive Ingredients” Problem)

When the cost of production rises, companies pass those expenses to the consumer. For example:

- If global oil prices rise, transportation costs increase.

- If transport becomes expensive, the cost of delivering vegetables rises.

- Ultimately, you pay more at the grocery store.

3. Monetary Inflation (The “Money Printer” Problem)

This is the most significant driver. If a government prints excessive currency to fund debt or public spending, the supply of money increases rapidly. When there is more paper money chasing the same amount of goods, the value of each individual unit drops, leading to higher prices.

Is Inflation Evil? The Surprising Truth

You might wonder why central banks don’t simply stop inflation to keep prices static. The truth is that zero inflation can be dangerous. If prices fall—a state known as deflation—people stop spending.

- Why buy a car today if it will be cheaper next month?

- Why invest in a home if construction costs are dropping?

When spending halts, businesses close and unemployment rises. Consequently, institutions like the Reserve Bank of India target a modest level of inflation (typically 2%–6%) to encourage economic activity. They want your money to lose a little value so that you spend or invest it rather than hoarding it.

The Real Impact: Winners and Losers

Inflation does not affect everyone equally. It creates a distinct divide between those who understand financial mechanics and those who do not.

The Losers:

- Savers: If your savings account earns 3% interest while inflation is 6%, you are effectively losing 3% of your wealth annually.

- Fixed Income Earners: Pensioners and those on static salaries struggle as the cost of living rises while their income remains stagnant.

The Winners:

- Borrowers: Inflation erodes the real value of debt. If you took a large loan years ago, paying it back today is easier because your income has likely risen with inflation.

- Asset Owners: Those who hold real estate, gold, or equities often see their asset values rise in tandem with inflation.

How Do You Beat Inflation?

You cannot stop inflation, but you can certainly outrun it. The golden rule of personal finance is simple: To build wealth, your money must grow faster than inflation eats it.

If inflation is 6%, consider your options:

- Cash at Home (0% return): You lose 6% of your wealth annually.

- Savings Account (3% return): You lose 3% of your wealth annually.

- Fixed Deposit (6-7% return): You barely break even.

- Investing (Stocks/Mutual Funds/Real Estate): By targeting 10-15% returns, you grow your wealth in real terms.

Final Thought: The Invisible Tax

Think of inflation as an invisible tax on those who do not understand how money works. It punishes those who play it “safe” with cash and rewards those who take calculated risks with investments.

Now that you understand what is inflation, you have a choice. You can let it slowly drain your hard-earned savings, or you can learn to invest and make inflation irrelevant. The choice is yours.

Quick Action Step:

Check the interest rate on your primary savings account. If it is lower than 6%, your money is losing value every single day. In our next article, we will discuss compound interest—the most powerful weapon you have to fight back against inflation.