When you walk into an electronics store, you are often greeted by a tempting offer: no cost emi hidden charges are non-existent, or so the marketing claims suggest. It sounds like a dream deal where you pay the price of the product divided by the number of months, with zero interest.

However, in the world of personal finance, if something sounds too good to be true, it usually is. Understanding the reality of these schemes is vital for effective money management. Let us peel back the layers of this financial marketing strategy.

The Truth Behind the Marketing

The concept of no cost emi hidden charges is a clever psychological play. Banks and retailers want to lower the barrier to entry for high-ticket items. By removing the “interest” label, they make the purchase feel painless.

In reality, the interest is almost always built into the price. You are simply paying the interest upfront through a discounted price that you no longer receive. Here is how the math actually works against your wallet.

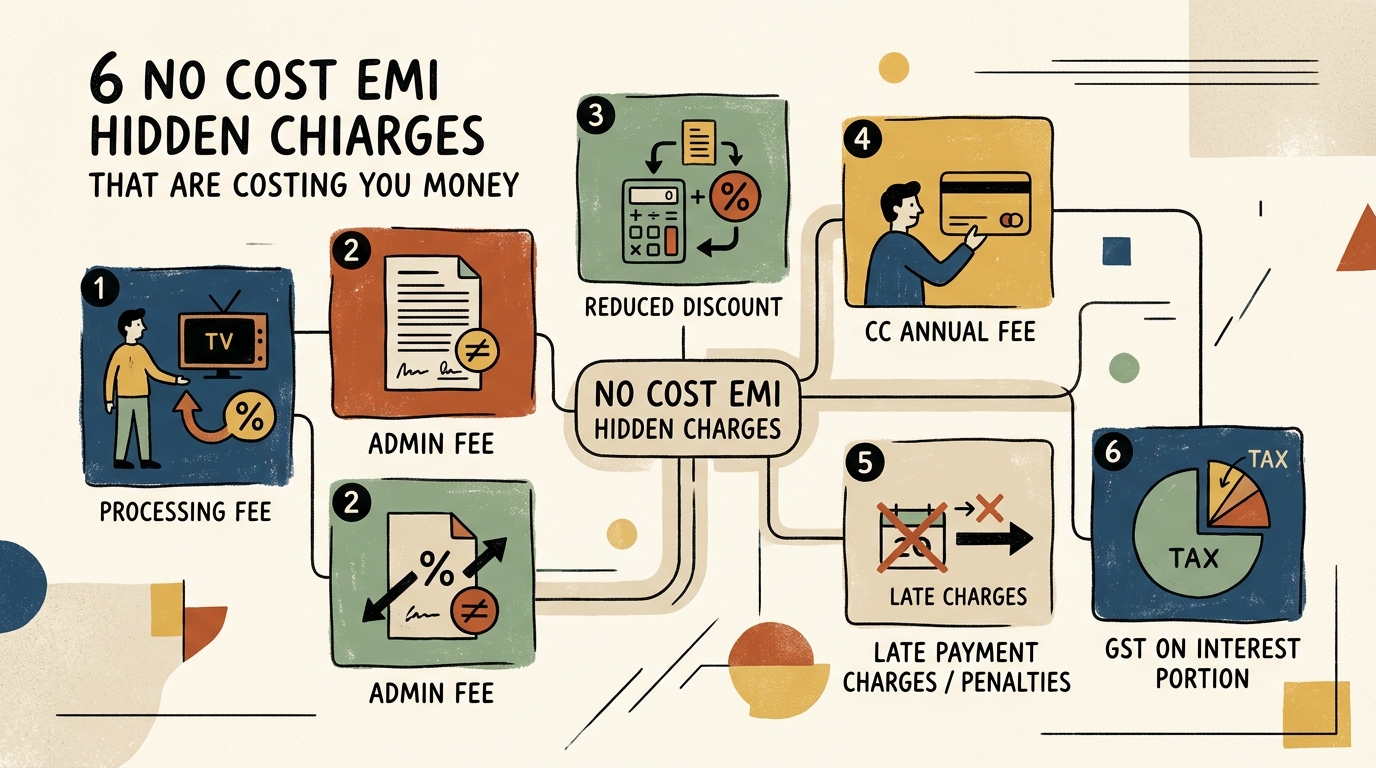

1. The Processing Fee Trap

Even if the interest rate is zero, banks rarely provide services for free. Most lenders charge a processing fee for every EMI transaction. This fee can range from ₹199 to ₹999 plus applicable taxes.

If you are buying a budget smartphone for ₹15,000, a processing fee of ₹500 effectively adds over 3% to your cost. This is a classic example of no cost emi hidden charges that most shoppers ignore until they see their credit card statement.

2. GST on Interest Components

The government mandates a Goods and Services Tax (GST) on all financial services. Even if the retailer claims to bear the interest, the bank will charge GST on the processing fee and sometimes on the interest component itself.

You must remember that GST is currently 18% in India. When you calculate the no cost emi hidden charges, you must include this 18% tax on every fee the bank levies. This turns a “zero interest” deal into a taxable expense.

3. Forfeiture of Cash Discounts

This is the most significant hidden cost. When you opt for a “No Cost” plan, the retailer often disqualifies you from the instant cash discount or bank cashback offers available to those who pay in full.

If a laptop is priced at ₹50,000 but has a ₹5,000 instant discount for full payment, choosing the EMI option means you pay the full ₹50,000. That ₹5,000 difference is effectively the interest you are paying, proving that no cost emi hidden charges are simply disguised as lost opportunities.

4. The Impact of Late Payment Penalties

If you miss a single EMI payment, the “No Cost” benefit vanishes instantly. Banks will then apply a high interest rate, often ranging from 36% to 42% per annum, on the outstanding amount.

Additionally, you will be hit with a late payment fee and a penalty on your credit score. To learn more about how these rates are regulated, visit the Reserve Bank of India guidelines on credit products.

5. Impact on Credit Utilization Ratio

Every EMI transaction blocks a portion of your credit limit. If you have multiple “No Cost” EMIs running, your credit utilization ratio spikes, which can negatively impact your credit score.

Maintaining a high credit score is essential for future loans like home or car loans. Ignoring the no cost emi hidden charges might save you a few thousand rupees today but could cost you lakhs in higher interest rates on future loans due to a lowered credit score.

6. The Hidden Cost of Documentation

Some lenders charge a “documentation fee” or “file handling charge” for EMI conversions. While these amounts seem small, they contribute to the total cost of ownership.

When you aggregate these small fees, the total no cost emi hidden charges can make the product significantly more expensive than its market value. Always read the fine print before clicking the “Convert to EMI” button.

Final Verdict on EMI Schemes

Are these schemes ever worth it? They can be useful if you have the cash but want to maintain liquidity for emergencies. However, you must account for the no cost emi hidden charges before committing.

Always calculate the total outflow. If the total of your EMIs plus fees exceeds the discounted cash price, you are losing money. Stay vigilant, read the terms, and avoid falling for the “No Cost” myth.

By being aware of no cost emi hidden charges, you protect your financial health. Never let convenience override your mathematical judgment when managing your personal finances.

Ultimately, the best way to buy is to save up and pay in full. This avoids all no cost emi hidden charges and often allows you to negotiate a better price with the retailer.

Understanding no cost emi hidden charges is the first step toward financial freedom. Keep your credit clean and your expenses transparent.