Understanding the financial landscape in India requires a deep dive into the mechanisms that govern our economy. If you have ever wondered what is repo rate, you are looking at the single most influential lever in the Indian banking system.

The repo rate acts as the master interest rate. It dictates the cost of borrowing for commercial banks, which in turn ripples down to your personal finances. Even a small adjustment, such as a 0.5% hike, can have profound long-term consequences on your debt obligations.

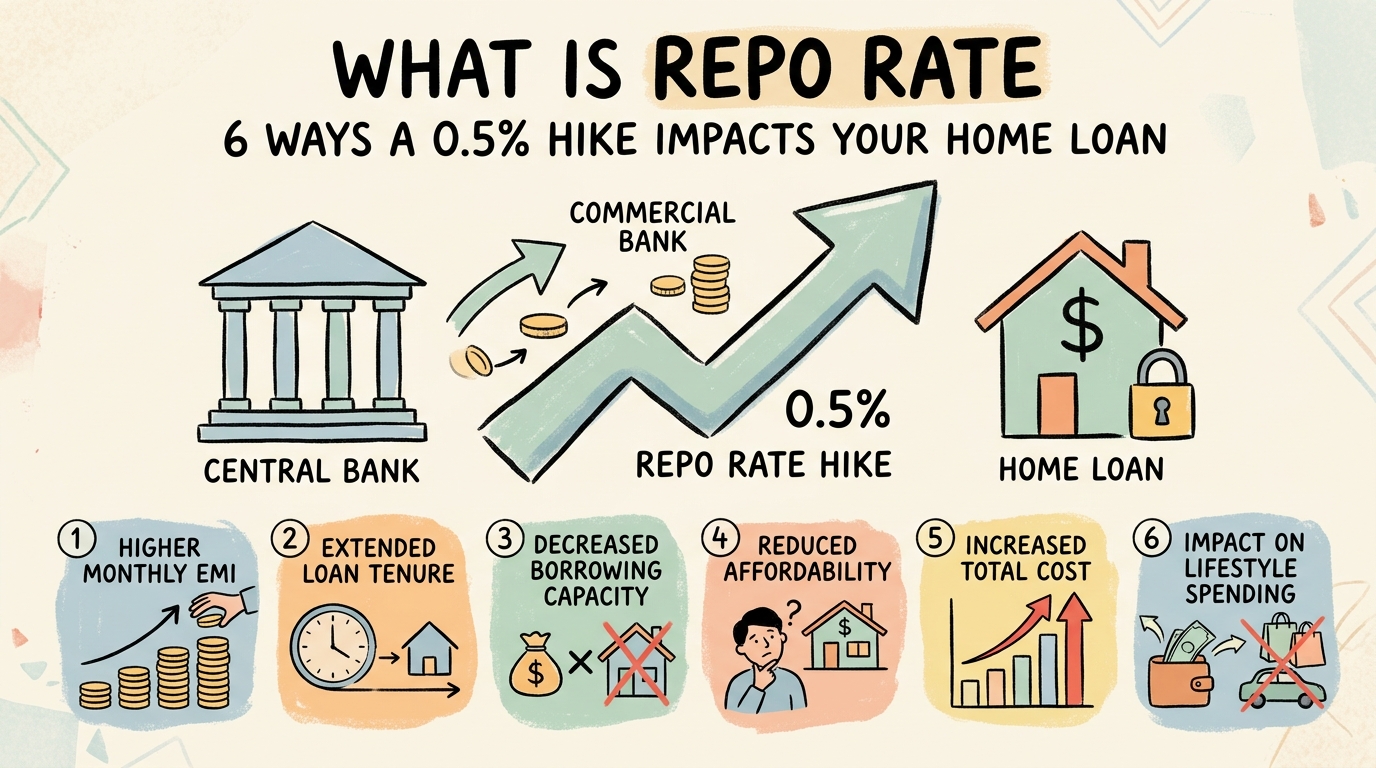

The Mechanics of the Repo Rate

At its core, the repo rate is the interest rate at which the Reserve Bank of India lends money to commercial banks. When banks face a liquidity crunch, they borrow from the central bank. By increasing this rate, the RBI makes it more expensive for banks to borrow funds.

Consequently, banks pass this increased cost onto consumers. Whether you are looking for a car loan or a home loan, the interest rates you pay are directly tied to these policy decisions. Mastering money management begins with understanding these macroeconomic shifts.

1. How the Repo Rate Influences Your Home Loan

Most home loans in India are linked to an External Benchmark Lending Rate (EBLR), which is directly pegged to the repo rate. When the RBI announces a hike, your bank typically updates your interest rate within a few weeks. This adjustment happens automatically, often without a formal notification.

If your home loan interest rate increases, your EMI or your loan tenure must adjust to compensate. Banks generally prefer to extend the tenure of the loan rather than increasing the EMI significantly, as this keeps the monthly payment affordable for the borrower.

2. The Hidden Cost of a 0.5% Rate Hike

Many borrowers underestimate the impact of a seemingly small 0.5% increase. However, the math behind what is repo rate reveals a harsh reality. If you have a home loan of ₹50,00,000 with 20 years remaining, a 0.5% hike can extend your tenure by several years.

Over the life of a long-term loan, this small percentage point increase can result in paying several lakhs of rupees in additional interest. This is why financial experts emphasize the importance of tracking policy announcements closely.

3. Strategies to Mitigate Interest Rate Volatility

Since you cannot control the RBI, you must control your debt structure. One effective strategy is to make periodic prepayments toward your principal amount. By reducing the principal, you minimize the interest burden, even if the repo rate rises.

Another approach is to maintain an emergency fund that covers at least six months of EMIs. This ensures that even if your interest costs rise, you do not default on your payments. Understanding what is repo rate allows you to plan your finances proactively rather than reactively.

4. Why the RBI Adjusts the Repo Rate

The primary goal of the RBI in adjusting the repo rate is to control inflation. When there is too much money circulating in the economy, prices rise. By raising the repo rate, the RBI encourages saving and discourages borrowing, which cools down demand.

Conversely, when the economy needs a boost, the RBI lowers the repo rate to make credit cheaper. This cycle of tightening and easing is essential for maintaining price stability and economic growth in India.

5. Impact on Savings and Fixed Deposits

It is not all bad news for consumers. When the repo rate rises, banks also increase the interest rates offered on Fixed Deposits (FDs) and savings accounts. If you are a net saver, you benefit from higher returns on your capital.

However, the increase in FD rates often lags behind the increase in loan rates. This is why it is vital to monitor the financial news to understand what is repo rate and how it affects your specific financial portfolio.

6. The Long-Term Outlook for Borrowers

Borrowers should view their home loans as dynamic rather than static contracts. Because what is repo rate is a fluid concept, your loan agreement is essentially a variable-rate instrument. You must be prepared for periods of high-interest environments.

Always review your loan statement annually. If you find that your tenure has extended significantly due to rate hikes, consider switching your loan to a lender offering better terms or increasing your EMI voluntarily to shorten the tenure.

Conclusion: Staying Informed

Understanding what is repo rate is not just for economists; it is a fundamental skill for every Indian borrower. By recognizing how the RBI’s decisions impact your home loan, you can take control of your financial future.

Whether it is a 0.5% hike or a cut, staying informed helps you make better decisions regarding your debt and savings. Remember, what is repo rate is the heartbeat of the Indian economy, and tracking it is the first step toward financial freedom.

As you continue to navigate your financial journey, keep an eye on how these rates shift. Knowing what is repo rate empowers you to manage your home loan effectively, ensuring that a 0.5% increase does not derail your long-term goals.

Ultimately, what is repo rate serves as a reminder that your personal finances are inextricably linked to the broader economic environment. Stay vigilant, stay informed, and manage your debt wisely.