Navigating the complexities of Indian tax laws can often feel overwhelming, especially when it comes to interest income. Many taxpayers are unaware that they can legally reduce their tax liability on interest earned from banks and post offices. Understanding the nuances of section 80TTB vs 80TTA is essential for anyone looking to optimize their tax savings.

Whether you are a young professional or a senior citizen, these sections offer specific deductions that can significantly lower your taxable income. By leveraging these provisions, you can keep more of your hard-earned money. If you are interested in broader money management strategies, it is vital to start with these foundational tax-saving tools.

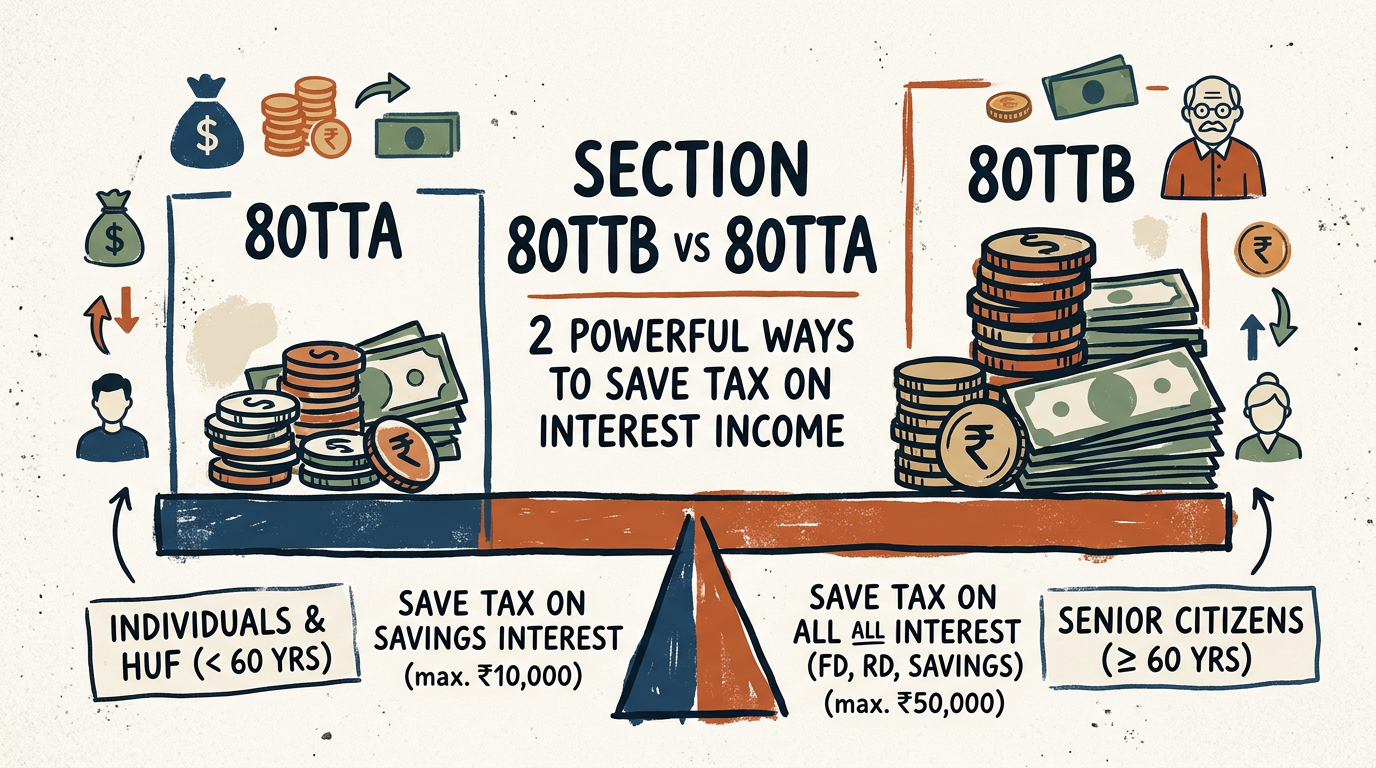

Understanding the Basics of Tax Deductions on Interest

The Income Tax Act, 1961, provides specific provisions to encourage savings. Interest earned on savings accounts and fixed deposits is generally considered ‘Income from Other Sources’ and is taxable at your slab rate. However, the government introduced specific sections to provide relief to different categories of taxpayers.

The core difference between section 80TTB vs 80TTA lies in the eligibility criteria and the maximum deduction limit. While one is designed for the general public, the other is a special benefit for the elderly. Knowing which one applies to you is the first step toward effective tax planning.

1. Who Qualifies Under Section 80TTA?

Section 80TTA is specifically designed for individual taxpayers and Hindu Undivided Families (HUFs). It applies to anyone who is not a senior citizen. This section provides a deduction on interest earned from savings accounts held with banks, cooperative societies, or post offices.

The maximum deduction allowed under this section is ₹10,000 per financial year. If your total interest income from all your savings accounts is less than ₹10,000, the entire amount is deductible. If it exceeds this limit, you must pay tax on the excess amount.

It is important to note that this deduction does not apply to interest earned on fixed deposits, recurring deposits, or any other time deposits. It is strictly limited to savings account interest. For detailed regulatory updates, you can always refer to the Reserve Bank of India guidelines.

2. Who Qualifies Under Section 80TTB?

Section 80TTB is a dedicated provision for senior citizens in India. A senior citizen is defined as any individual who is 60 years of age or older at any time during the financial year. This section is much more generous than its counterpart.

Under this provision, senior citizens can claim a deduction of up to ₹50,000 per financial year. Unlike 80TTA, this deduction covers interest from savings accounts, fixed deposits, recurring deposits, and other time deposits held with banks or post offices.

This is a massive benefit for retirees who rely on interest income for their daily expenses. By utilizing section 80TTB vs 80TTA correctly, senior citizens can effectively shield a significant portion of their passive income from the tax net.

Key Differences You Must Know

When comparing section 80TTB vs 80TTA, the most significant difference is the scope of the deduction. While 80TTA is restricted to savings accounts, 80TTB covers almost all interest-bearing instruments offered by banks and post offices.

Furthermore, the deduction limit under 80TTB is five times higher than that of 80TTA. This reflects the government’s intent to provide greater financial security to the elderly population. It is also important to remember that you cannot claim both deductions simultaneously.

If you are a senior citizen, you are ineligible to claim deductions under 80TTA. You must exclusively use 80TTB. Conversely, if you are under 60, you must rely on 80TTA for your savings account interest deductions.

Strategic Tips for Tax Optimization

To make the most of section 80TTB vs 80TTA, you should maintain clear records of your interest certificates provided by your bank. These documents are crucial when filing your Income Tax Return (ITR).

If you are a senior citizen, ensure your bank has updated your status in their records to avoid unnecessary TDS (Tax Deducted at Source) on your fixed deposits. Submitting Form 15H can further help in preventing TDS if your total income is below the taxable limit.

For those under 60, keep track of the interest earned across multiple savings accounts. Since the limit of ₹10,000 is aggregate, you must calculate the total interest from all accounts before claiming the deduction. Mastering section 80TTB vs 80TTA is a simple yet effective way to optimize your annual tax outgo.

In conclusion, understanding section 80TTB vs 80TTA is vital for every taxpayer. By identifying your eligibility and limits, you can ensure that you are not paying more tax than necessary. Always stay updated with the latest changes in the Income Tax Act to keep your finances in order.