Navigating the complex landscape of Indian taxation can be daunting, but understanding section 80D deductions is a powerful way to optimize your financial health. By strategically utilizing these provisions, you can significantly reduce your taxable income while ensuring robust medical protection for your family.

Effective money management is not just about earning; it is about keeping more of what you earn through legal tax planning. This guide breaks down everything you need to know about maximizing your tax savings through health insurance.

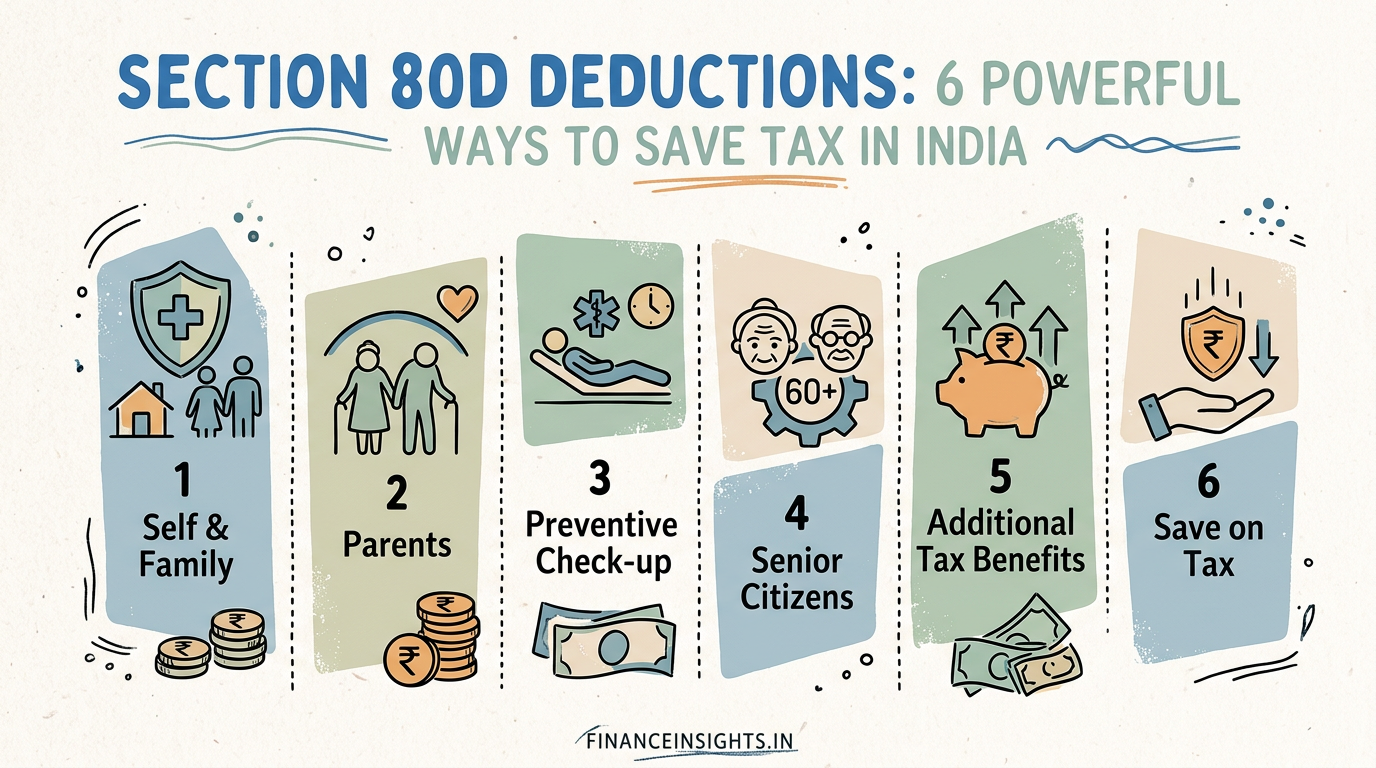

Understanding the Basics of Section 80D

The Income Tax Act provides section 80D deductions to encourage citizens to secure health insurance. This deduction is available to individuals and Hindu Undivided Families (HUFs) for premiums paid toward health insurance policies.

It is important to note that premiums must be paid via non-cash modes, such as net banking, credit cards, or cheques, to be eligible. Cash payments are strictly excluded from these tax benefits.

1. Deductions for Yourself, Spouse, and Dependent Children

If you are below 60 years of age, you can claim section 80D deductions up to ₹25,000 for health insurance premiums paid for yourself, your spouse, and dependent children. This limit includes any preventive health check-up costs, capped at ₹5,000 within this overall limit.

For example, if you pay a premium of ₹20,000 and spend ₹6,000 on check-ups, your total deduction is limited to ₹25,000. Proper documentation is essential for all claims.

2. Additional Benefits for Senior Citizen Parents

If you pay health insurance premiums for your parents who are senior citizens (aged 60 or above), you can claim an additional deduction of up to ₹50,000 under section 80D deductions. This is a significant relief for those supporting elderly family members.

Even if your parents are not dependent on you, you can still claim this benefit. It is a separate bucket from your own personal insurance deduction, allowing for a combined potential deduction of ₹75,000.

3. The Special Provision for Very Senior Citizens

For parents who are very senior citizens (aged 80 or above) and do not have health insurance, the government allows a deduction for medical expenditure. You can claim up to ₹50,000 for medical bills incurred for them under section 80D deductions.

This ensures that even those who cannot obtain insurance due to age or pre-existing conditions are not left out of the tax-saving net. Always keep original invoices and prescriptions as proof.

4. Understanding the Preventive Health Check-up Limit

Many taxpayers overlook the preventive health check-up component of section 80D deductions. You can claim up to ₹5,000 for these check-ups, which is inclusive of the total limit for the family member category.

This encourages proactive healthcare. Whether it is a routine blood test or a full-body scan, these costs help you lower your tax liability while monitoring your well-being.

5. Why Non-Cash Payments are Mandatory

To ensure transparency, the Income Tax Department mandates that section 80D deductions are only valid for payments made through banking channels. This rule is strictly enforced by the Reserve Bank of India regulated payment systems.

Avoid paying premiums in cash, as these will be disallowed during tax assessment. Always use digital payment methods to maintain a clear audit trail of your financial transactions.

6. Combining Deductions for Maximum Impact

The true power of section 80D deductions lies in stacking these limits. A taxpayer below 60 can claim ₹25,000 for their own family and ₹50,000 for senior citizen parents, totaling ₹75,000 in deductions.

If the taxpayer is also a senior citizen, the limits increase further. Planning these payments well before the financial year ends is crucial for effective tax optimization.

Conclusion: Start Planning Today

Mastering section 80D deductions is an essential skill for every taxpayer in India. By staying informed and paying your premiums through the correct channels, you can protect your family and your wealth simultaneously.

Remember, tax laws are subject to change, so it is always wise to consult with a certified financial advisor. Start your journey toward smarter tax planning today and secure your financial future.