Understanding what is NAV in mutual fund investments is the first step toward becoming a savvy investor. Many beginners mistakenly believe that a lower Net Asset Value (NAV) makes a fund “cheaper” or a better bargain. This is a common myth that can lead to poor investment decisions.

Think of a mutual fund like a giant pizza. The entire fund is the pizza, and the NAV represents the price of a single slice. Whether you buy a slice from a pizza cut into eight pieces or sixteen pieces, you are still buying the same amount of food relative to the total value. Let’s dive deep into this concept.

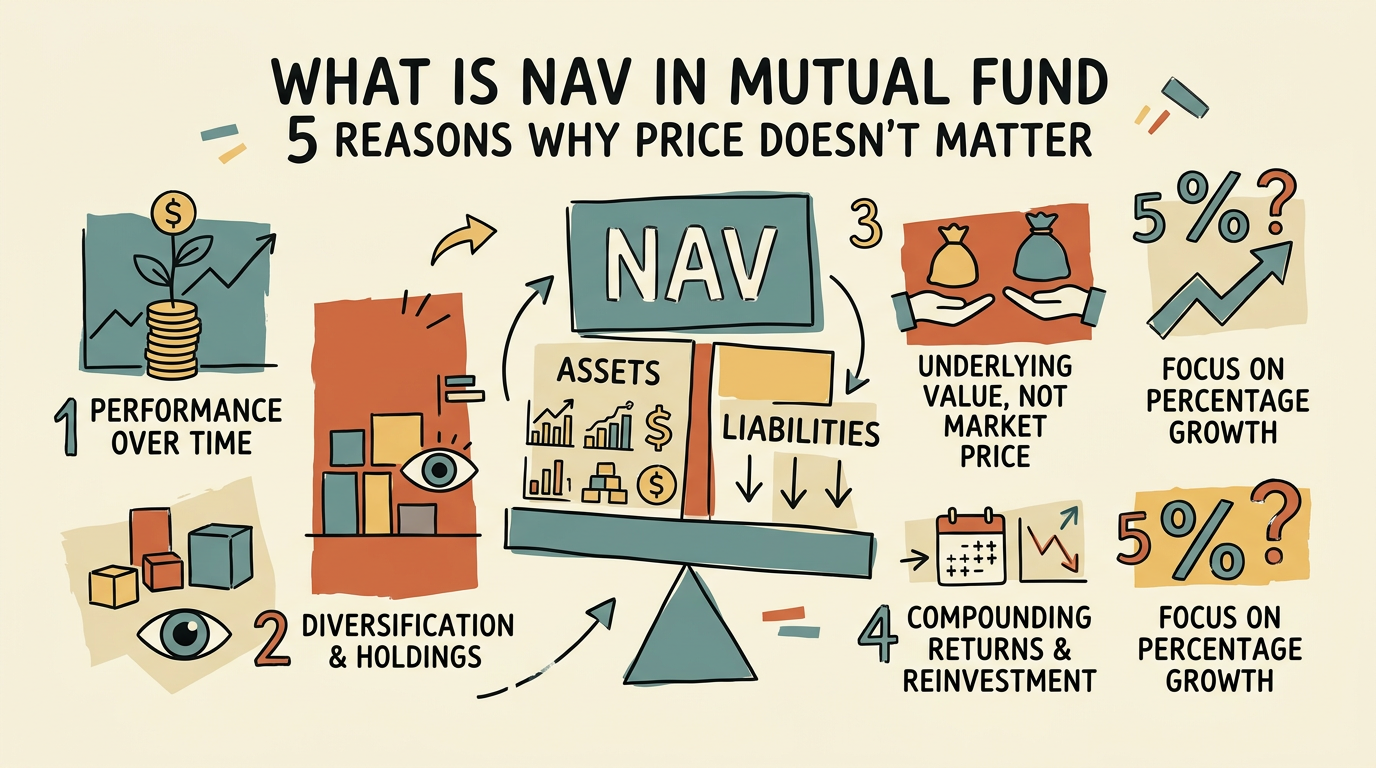

What is NAV in mutual fund?

In simple terms, what is NAV in mutual fund jargon refers to the per-unit market value of the scheme. It is calculated by taking the total value of all the assets held by the fund, subtracting the liabilities, and dividing that figure by the total number of units issued to investors.

The Reserve Bank of India provides guidelines that help maintain transparency in financial markets, ensuring that investors understand how these valuations are derived. When you invest, you are essentially purchasing units at this specific price.

1. How NAV is calculated daily

The calculation of NAV happens at the end of every trading day. Since the underlying stocks or bonds in the portfolio fluctuate in price, the total value of the fund changes constantly. If you want to master money management, you must track how these daily changes impact your portfolio.

The formula is: (Total Assets – Total Liabilities) / Total Number of Outstanding Units. This ensures that the price you pay is always reflective of the current market value of the underlying securities.

2. Why a lower NAV is not necessarily better

A common misconception is that a fund with an NAV of ₹10 is “cheaper” than a fund with an NAV of ₹100. This is fundamentally incorrect. What is NAV in mutual fund performance is not determined by the price per unit, but by the performance of the underlying assets.

If you invest ₹10,000 in a fund with an NAV of ₹10, you get 1,000 units. If you invest the same amount in a fund with an NAV of ₹100, you get 100 units. If both funds grow by 10%, your investment value becomes ₹11,000 in both cases.

3. The role of expense ratios

When asking what is NAV in mutual fund analysis, you must also consider the expense ratio. This is the fee the fund house charges to manage your money. The NAV is calculated *after* deducting these expenses.

A fund with a high expense ratio will have a lower NAV than it would have had otherwise. Therefore, focusing solely on the NAV ignores the crucial impact of management fees on your long-term returns.

4. NAV vs. Stock Price

Investors often confuse NAV with stock prices. Unlike a stock, where the price is determined by demand and supply, what is NAV in mutual fund structures is determined purely by the value of the underlying assets.

You cannot “trade” mutual fund units throughout the day like stocks. You buy or sell them at the end-of-day NAV, which removes the volatility associated with intraday market fluctuations.

5. Why NAV should not be your primary metric

If you are choosing a fund based on its NAV, you are likely making a mistake. Experienced investors look at the portfolio quality, the fund manager’s track record, and the risk-adjusted returns.

What is NAV in mutual fund decision-making? It is merely a tool to track your unit holding, not a performance indicator. A fund with a high NAV might actually be a very successful fund that has grown significantly over many years.

In summary, stop worrying about whether an NAV is high or low. Focus on your financial goals, the fund’s consistency, and your risk appetite. Understanding what is NAV in mutual fund mechanics allows you to ignore the noise and focus on what truly builds wealth over time.

Always remember that what is NAV in mutual fund calculations is just a reflection of the past performance of the underlying assets. It does not predict future gains. Keep your investment strategy simple, stay disciplined, and let the power of compounding work for you.